TL;DR: Yes, foreigners can buying property in Singapore; no special approval needed. Landed houses and HDB flats are mostly off limits. The catch is the 60% Additional Buyer’s Stamp Duty on top of the purchase price, plus regular Buyer’s Stamp Duty. Banks will still give you a mortgage, just expect a lower loan amount and a bit more paperwork. Talk to a local agent before you fall in love with a unit, it’ll save you money and stress.

If you’ve been eyeing a home in Singapore and typing “can foreigners buying property in Singapore” into Google at midnight, you’re not alone. It’s one of the first questions almost every overseas buyer asks us at SG Luxury Condo, usually right after “which neighbourhood should I even be looking at?”

The good news is that the answer isn’t complicated once someone walks you through it properly. The confusing part is that most of what’s online mixes up rules for citizens, Permanent Residents, and foreigners, and doesn’t tell you what it actually costs to buy as a non-resident. So let’s clear that up here, in plain English, without the legal jargon.

The Short Answer: Yes, Foreigners Buying Property in Singapore

Foreigners are allowed to buy private condominiums and apartments in Singapore without needing any special government approval. This has been the case for years and hasn’t changed. What you can’t do freely is buy landed houses (think terrace houses, bungalows, semi-detached homes) or HDB flats, which are Singapore’s public housing. Those come with restrictions that make them impractical for most overseas buyers anyway.

So if your plan is a condo, and for most foreign buyers it is, you’re in good shape. This is actually one reason why luxury condos for sale in Singapore have become such a popular entry point for foreign investors and expats. It’s the one property category where ownership is genuinely straightforward.

What Foreigners Can and Can’t Buy: The Breakdown

Here’s how it actually splits, based on Singapore’s Residential Property Act.

You can buy without approval:

- Private condominiums and apartments (any size, any launch)

- Executive condominiums, but only once they’re more than 10 years old

- Strata landed homes within approved condo developments, like some units in Sentosa Cove

- Leasehold landed property with a lease of 7 years or less

You’ll need approval from the Singapore Land Authority (SLA):

- Landed houses such as bungalows, terrace houses, and semi-detached homes on the mainland

- Vacant residential land

You generally can’t buy at all:

- HDB flats, unless you’re married to a Singapore citizen and meet other conditions

- Good Class Bungalows (GCBs), except under very rare circumstances tied to significant economic contribution

Sentosa is the one exception worth knowing. It’s the only part of Singapore where foreigners can buy landed homes without prior SLA approval, which is part of why Sentosa Cove bungalows attract so much overseas interest.

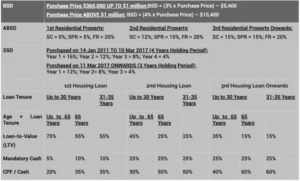

The Real Cost: ABSD and Stamp Duty for Foreign Buying property in Singapore

This is the part most people underestimate, and honestly, it’s the number that changes the whole conversation. On top of the price of the property, every buyer in Singapore pays Buyer’s Stamp Duty (BSD), and foreigners also pay Additional Buyer’s Stamp Duty (ABSD) on top of that.

Buyer Profile | ABSD Rate (2026) |

Singapore Citizen, 1st property | 0% |

Singapore Citizen, 2nd property | 20% |

Permanent Resident, 1st property | 5% |

Permanent Resident, 2nd property | 30% |

Foreigner (non-PR) | 60% |

Nationals of the US, Switzerland, Liechtenstein, Norway, Iceland | 0% (under free trade agreement terms) |

Yes, 60% is a big number, and it applies regardless of how many properties you already own here. It’s the biggest single factor in your budget planning, and it’s exactly why we always recommend foreign buyers speak to a proper Singapore property investment advisor before they start browsing listings, not after they’ve already fallen in love with a unit. Getting the tax math right at the start saves a lot of headaches later.

A few nationalities get a break here. Buyers from the US, Switzerland, Liechtenstein, Norway, and Iceland pay the same rate as a Singapore citizen would, thanks to free trade agreements. Worth checking if you qualify before you assume the worst.

Buyer’s Stamp Duty is a smaller, tiered cost that everyone pays regardless of nationality, ranging from 1% to 6% depending on the purchase price. It’s not the deal-breaker ABSD can be, but it still needs to be in your budget.

Financing: Can Foreigners Get a Mortgage in Singapore?

Yes, and Singapore banks are generally quite comfortable lending to foreign buyers, though the terms are a bit tighter than what locals get. Here’s roughly what to expect:

- Loan-to-value (LTV) ratio typically sits between 60% and 75%, meaning you’ll need 25% to 40% in cash or CPF (if applicable) upfront

- Interest rates for foreigners can run slightly higher than for citizens or PRs

- Banks will look closely at your income, employment stability, and existing debt obligations

- ABSD and BSD must be paid fully in cash upfront, they can’t be financed through your home loan

If you’re not planning to finance and intend to pay in cash, this whole process moves a lot faster. Either way, it’s worth getting a mortgage in-principle approval before you start viewing units seriously, so you’re not negotiating on a property you can’t actually finance.

How the Buying Process Actually Works, Step by Step

- Set your budget including ABSD, BSD, legal fees, and agent commission, not just the sticker price of the unit

- Get pre-approved for financing if you’re taking a loan, so you know your real spending power

- Shortlist properties with a property agent in Singapore who understands what foreign buyers can and can’t purchase, this avoids wasted time on ineligible listings

- View units and negotiate the price and terms with the seller or developer

- Pay the Option Fee (usually 1% to 5% of the price) to secure an Option to Purchase (OTP)

- Exercise the option within the agreed period, typically 2 weeks, paying the balance deposit

- Engage a conveyancing lawyer to handle the Sale and Purchase Agreement and title transfer

- Complete the transaction, pay remaining stamp duties, and collect your keys

New launch purchases follow a slightly different, more regulated process through the developer, but the core idea is the same.

Where Foreigners Buying Property in Singapore

There’s no single “right” district, but certain areas come up again and again with our foreign clients. Orchard and River Valley remain popular for their central location and prestige. The Core Central Region attracts investors chasing capital appreciation and rental demand from expats. Sentosa Cove is the obvious pick for anyone specifically wanting a landed home by the water. And districts near good international schools, like Bukit Timah and Holland Village, tend to draw families relocating for work.

If you’re still weighing up whether Singapore property is the right investment for you at all, our piece on why foreigners are buying property in Singapore digs into the actual motivations we’re seeing on the ground, beyond just the tax numbers.

Is the 60% ABSD Worth It?

This is the honest question everyone eventually asks, and it deserves an honest answer. For some buyers, yes. Singapore’s political stability, strong currency, transparent legal system, and consistent long-term capital growth make it a market where the upfront cost can pay off over a 5 to 10 year horizon, especially with prime freehold condos that hold value well.

For others, particularly short-term speculators, the 60% ABSD makes the math much harder to justify. There are also legitimate ways to reduce your exposure depending on your structure and nationality, which is a conversation worth having with a specialist rather than guessing. If you want the mechanics spelled out, our guide on how to avoid overpaying on ABSD walks through the legal options available to foreign buyers.

Final Thoughts

Buying property in Singapore as a foreigner isn’t complicated once you understand the rules, but it’s also not a market where guessing your way through it is a good idea. Between ABSD calculations, financing limits, and picking the right district and unit type, a lot of foreign buyers end up overpaying or missing better options simply because nobody walked them through it properly.