Most parents who look into buy property under trust in Singapore are chasing one thing. They want to dodge ABSD on a second property, and someone told them a trust could do it.

It still can. But the rules changed hard in 2023, and a lot of the advice floating around online is now outdated. Before you sign anything, here’s what actually applies today.

TL;DR

ABSD (Trust) is 65% upfront on any residential property transferred into a living trust, as of 27 April 2023.

You can apply for a refund of the difference if the beneficiary is clearly named, a Singapore Citizen, owns no other property, and the trust is irrevocable.

Buy property under trust is still one of the few legal ways to secure a property for a child without triggering ABSD, once remission is approved.

No bank will lend against a trust property held for a minor. You’ll need to fund it fully or use another asset as collateral.

Decoupling often works out cheaper than a trust if you already co-own a property with your spouse. Trust makes more sense in specific situations, not as a default move.

Get the Trust Deed and Option to Purchase wording right, or you risk paying 65% ABSD with no way to claw it back.

What Does Buy Property Under Trust Actually Mean?

A trust splits ownership into two parts. One person, the trustee, is registered as the legal owner. Another person, the beneficiary, actually owns the benefits.

Think of it like CPF. The CPF Board holds your retirement savings as trustee, but you’re the one who benefits from it. Property trusts work the same way, just applied to a condo or landed home instead of a savings account.

Parents typically set this up to buy a home in a child’s name. The child, usually under 21, becomes the beneficiary. The parent acts as trustee, handling the paperwork, the taxes, and the property management, while the ownership itself legally belongs to the child.

Trustee vs Beneficiary: Who’s Responsible For What

Legal owner of the property, entitled to all rental income and sale proceeds

The trustee doesn’t own the property in any real sense. They manage it. Every dollar of rent, every cent from a future sale, belongs to the beneficiary, not the trustee. That distinction matters more than most people realise, especially when it comes to bank loans (more on that below).

A trust deed spells all of this out. It should name the trustee and beneficiary clearly, describe the property, and set out the trustee’s powers, including the ability to rent, sell, or reinvest on the beneficiary’s behalf. Lawyers draft this, not property agents, so budget for legal fees from the start.

The 65% ABSD (Trust) Rule, and How Remission Actually Works

This is the part that trips up almost everyone.

Since 9 May 2022, transferring residential property into a living trust triggers ABSD. The rate started at 35% and jumped to 65% on 27 April 2023. That’s payable upfront, in full, regardless of who the beneficiary is.

The government did this specifically to stop people using trusts to flip property and dodge ABSD without any real intention of holding it long-term.

Here’s the part that actually matters for genuine buyers: you can apply for a remission (a refund) of the difference between 65% and the ABSD rate that would normally apply to your beneficiary, provided you meet IRAS’s conditions.

ABSD (Trust) Remission Checklist

To qualify for a refund, all of the following need to be true:

The beneficiary is named explicitly in the trust deed, not left vague or “to be determined.”

The beneficiary is an identifiable individual, and beneficial ownership has already vested in them at the time of transfer.

The trust is irrevocable. You can’t build in a clause letting yourself reverse or change the beneficiary later.

The beneficiary isn’t subject to any condition that could still change their ownership (no “if X happens” clauses).

Where the beneficiary is a first-time property owner with no other residential property, the refund typically brings the effective ABSD down close to 0%.

The application has to go to IRAS within 6 months of executing the instrument. Miss that window and the 65% simply stays paid, no exceptions.

VERY IMPORTANT. Get the Trust Deed drafted properly before you exercise the Option to Purchase, and get it stamped in the correct sequence. A poorly worded deed, or one that gives you (the settlor) any right to revoke it, will get the remission application rejected outright, no matter how good your intentions were.

Step-by-Step: How to Buy Property Under Trust

Most buyers are in this situation, where the trust isn’t set up yet at the point of purchase.

The Option to Purchase (OTP) is issued to the individual(s) buying, without stating trust capacity.

After the option is issued but before it’s exercised, the purchaser executes the declaration of trust and gets it stamped.

When exercising the option, the purchaser writes in to declare they’re exercising it in a trust capacity, attaching the trust deed and stamp certificate.

There’s technically no need to amend the Sale and Purchase Agreement at this stage.

The OTP itself gets filled in a specific way: (Trustee Name) in her/his capacity as trustee for (Beneficiary Name). For example, “Mary Tan (NRIC no.) in her capacity as trustee for Baby Tan (Birth Cert no.).”

Get this sequence wrong, even by a few days, and IRAS may not accept the remission application. This is not a DIY job. Speak to a conveyancing lawyer or a consultant who’s actually done this before signing anything.

How Much Does It Cost to Buy Property Under Trust?

Item

Typical Cost

Trust Deed drafting

$8,000 – $10,000

Conveyancing fee

$2,000 – $3,000

ABSD (Trust), payable upfront

65% of purchase price or market value, whichever is higher

ABSD refund (if remission approved)

Reduces effective ABSD to match beneficiary’s actual profile

There’s no annual fee for the trust itself. You’ll still pay yearly property tax, and income tax if the unit is rented out, same as any other property.

Advantages of Buy Property Under Trust

No ABSD once remission is approved. If your child owns no other property, the trust property doesn’t trigger the tax that a second property normally would.

Locks in today’s prices. Property secured now for a child’s future, rather than whatever it costs when they’re old enough to buy it themselves.

Protection from creditors. If you go bankrupt years later, the property legally belongs to your child, not you, so creditors generally can’t touch it. (Note: gifts made within 5 years of bankruptcy can still be clawed back under the Bankruptcy Act.)

Not touched in a divorce. Since the trust property belongs to the child, it typically stays out of matrimonial asset division.

Simple estate planning tool. It’s a fairly clean way to pass on wealth without a complicated will.

Disadvantages of Buy Property Under Trust

No bank loan. Banks lend to the real owner, and a minor can’t legally sign loan documents. You’ll need to fund the purchase in cash, or use another fully-paid property as collateral to convince the bank.

You can’t take it back. Once the trust is set up, the property belongs to the child. There’s no “just in case” clause that lets you reclaim it later.

Counts against your child’s future purchases. When your child turns 21 and wants their own HDB flat or private property, this trust property counts as one they already own. Buying a second property later means they’ll pay ABSD themselves.

Blocks HDB eligibility. A child who owns private property (through a trust) generally can’t apply for a BTO or resale HDB flat unless they sell the private property first and serve the wait-out period.

65% cash outlay upfront, even with remission pending. You’re funding the full ABSD first and waiting for the refund, not paying a reduced amount from day one.

Trust vs Decoupling: Which Actually Saves More Money

Both are legal ways to reduce ABSD, but they solve different problems, and one is often cheaper.

Buying Under Trust

Decoupling

Best for

Securing a first property for a child

Freeing up one spouse to buy a 2nd property ABSD-free

Buyer’s Stamp Duty + conveyancing on the transferred share, roughly $20k-$25k for a mid-sized property

Reversible?

No

No, once done

Here’s a real example, based on a Singaporean couple with a $1.5 million property, $400,000 outstanding loan, and $200,000 CPF used, looking to buy a $1 million investment property.

Option 1, Trust route: Transfer current property to their son via trust, buy the new one directly. Cost of paying off the loan and CPF: $600,000, plus roughly $52,600 in Buyer’s Stamp Duty and conveyancing. Total: around $652,600.

Option 2, Decoupling: Cost comes to roughly $22,100.

In this case, decoupling wins by a wide margin. Trust tends to make more sense when:

You and your spouse have already decoupled and are eyeing a third investment property.

You own an HDB you intend to keep long-term (and want to avoid ABSD on the next purchase).

Your current property is close to fully paid off, so there’s minimal loan and CPF to unwind.

This really is case-by-case. Running your own numbers before committing to either path is worth the hour it takes.

Taxation on a Trust Property

The trustee, not the beneficiary, is billed for property tax and income tax, even though the child legally owns the asset.

Property tax: 4% for owner-occupied, 10% for rented out. (A common misconception is that trust property tax is 17%. It isn’t.)

Income tax: Rental income minus expenses, taxed at a flat 17%.

IRAS doesn’t care which bank account the rent lands in. Tax liability follows the registered owner (the trustee), not wherever the money physically sits.

When Does the Trust End?

The trust ends when the child turns 21, or when the conditions written into the trust deed are met, whichever comes first.

At that point, full ownership, including all mortgages and tax responsibilities, transfers cleanly to the child. If the property hasn’t hit 3 years post-CSC yet, it’s still advisable to formally transfer it, at a cost roughly equivalent to conveyancing a resale property (around $3,000).

One thing worth knowing upfront: a trust is a gift, not a loan. There’s no mechanism to “take it back” once it’s set up, even if your circumstances change.

Should You Buy Property Under Trust?

If the goal is genuinely securing your child’s future, whether that’s a home to grow into, a rental income stream for their education, or protection against your own business risk, buy property under trust remains one of the cleaner tools available in Singapore.

If the goal is purely to dodge ABSD with no real intention of the child benefiting, it’s worth being honest with yourself about that before you spend $10,000+ on legal fees. IRAS reviews these arrangements, and a trust set up purely as a workaround risks having the ABSD clawed back regardless of remission.

Buy property under trust is part of a broader wealth-building approach for a lot of the families we work with, which is why we built ourP.L.U.S wealth system around structuring property purchases the right way from the start. If you’re weighing trust against decoupling or another route entirely, it’s worth reading throughhow to legally avoid ABSD in Singapore before deciding, alongside our broader guide onhow to buy a condo in Singapore.

We handle both the Trust Deed and conveyancing under one roof, using a format that’s been structured specifically to meet IRAS’s remission conditions. If you’d like a second opinion on whether trust or decoupling fits your situation better, ourproperty consultation walks through your numbers directly, and ourSingapore property investment advisor can map out a longer-term strategy around it.

At SG Luxury Condo, we’ve helped clients navigate this from both sides, families securing a first home for their child and investors trying to structure a second or third property the smart way. If you’re browsingluxury condos for sale in Singapore and want to know whether a trust makes sense for your situation, reach out and we’ll walk through it together.

Advanced Heading

Frequently Asked Questions

Can I still buy property under trust in Singapore after the ABSD hike?

Yes. The 65% ABSD (Trust) is payable upfront, but you can apply for remission if the beneficiary is clearly named, a Singapore Citizen, and owns no other residential property. It’s still viable, just with more upfront cash needed and a tighter compliance process than before 2022.

Who actually pays the property tax on a trust property?

The trustee, based on the trustee’s status (owner-occupier or rental rate), not the beneficiary. IRAS bills the registered legal owner.

Can foreign parents be trustees for a Singaporean grandchild?

Yes, foreign parents or grandparents can act as trustee for a condo held in benefit of a Singaporean child. They can’t, however, buy landed property this way, as foreign ownership restrictions still apply.

Can I cancel a trust once it's set up?

No. Since the beneficiary is now the legal owner, the settlor has no right to unwind it. Some trust deeds include a clause attempting this, but courts tend to view that as evidence the trust isn’t genuine, which can create bigger problems with IRAS.

What happens if my child sells the property later?

The proceeds belong entirely to the beneficiary (your child), not you. As trustee, you manage the sale, but you have no legal claim over the money.

Can I be a trustee if I own an HDB that hasn't met MOP?

No. Acquiring private property to hold in trust during your HDB’s Minimum Occupation Period breaches the Housing and Development Act. HDB actively enforces this.

Does buying under trust affect my child's ability to get a BTO later?

Yes. Since the trust property is counted as owned by your child, they’ll need to sell it and serve the required wait-out period before applying for a BTO or resale HDB flat.

How is the OTP filled in if the trust isn't set up yet?

The option is issued to the purchaser individually, without stating trust capacity. The declaration of trust gets executed and stamped after the option is issued but before it’s exercised. Get the sequencing checked by a lawyer, since this is where remission applications most often go wrong.

Is buying under trust better than just gifting cash to my child later?

Not necessarily better, just different. A trust locks in today’s property prices and gives asset protection benefits a cash gift doesn’t. But it’s irreversible and comes with real upfront costs, so it depends on your actual goals, not a one-size-fits-all answer.

What's the biggest mistake people make when buy property under trust?

Treating it purely as an ABSD workaround without thinking through the loss of control, the loan restrictions, and the impact on the child’s future property eligibility. Trust works best when the underlying intent is genuinely about the child’s future, not just tax savings.

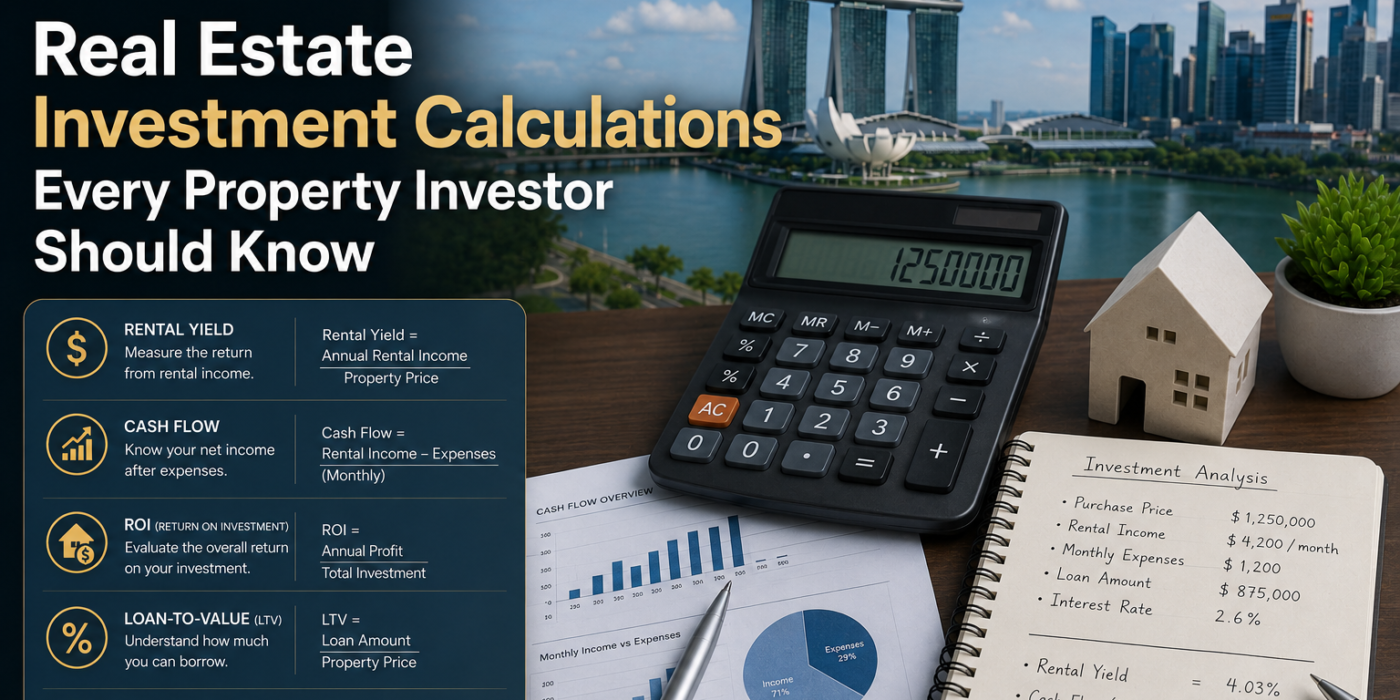

Most people who lose money on property didn’t pick a bad unit. They skipped the math.

That’s not an exaggeration. It’s what happens over and over when buyers get caught up in a showflat and forget the real estate investment calculations that would have told them the numbers didn’t work.

TL;DR

Real estate investment calculations aren’t complicated. Most of it is basic percentages, not advanced finance.

Check your TDSR and MSR before you view a single unit. It sets your real budget.

Gross yield is a quick filter. Net yield, DSCR, and cash-on-cash return tell you the real story.

The 1% rule is a rough screen, not a rule most Singapore condos will pass today.

Capital appreciation should be modelled conservatively, not off the best year the market ever had.

Run the full set of real estate investment calculations before you exercise the Option to Purchase, not after.

Why These Numbers Actually Matter Here

Property in Singapore runs on leverage. With a bank loan covering up to 75% of the price, your cash outlay is a fraction of the unit’s value. That’s exactly why the returns on your cash can look so much better than the returns on the property itself.

But leverage cuts both ways.

Get your real estate investment calculations wrong on a $1.5 million condo and you’re not looking at a rounding error. You’re looking at a five or six figure mistake. Add ABSD, TDSR limits, and monthly maintenance fees into the mix, and you’ll find the numbers Singapore investors actually use are quite different from what a generic American property blog will tell you.

Here’s what this guide covers, in the order most buyers should actually run them.

#

Calculation

What It Tells You

1

Downpayment & LTV

Cash and CPF you need upfront

2

Total Upfront Cash Outlay

Real cost including BSD, ABSD, legal fees

3

TDSR & MSR

Whether the bank will approve your loan

4

Net Rental Income

Actual monthly cash flow, not the headline rent

5

Gross Rental Yield

Quick way to shortlist properties

6

Net Rental Yield (Cap Rate)

Return after real costs are stripped out

7

The 1% Rule

Fast filter for rental-worthy units

8

Gross Rent Multiplier

Years of rent needed to cover the price

9

Debt Service Coverage Ratio

Whether rental income covers your loan

10

Cash-on-Cash Return

Return on the actual cash you put in

11

Payback Period

How long until you break even

12

Capital Appreciation

Long-term equity growth potential

13

Price Per Square Foot

Apples-to-apples comparison tool

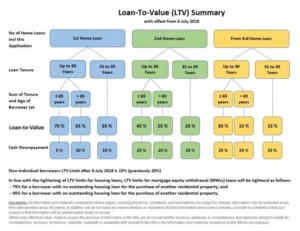

1. Downpayment and Loan-to-Value (LTV) Ratio

LTV-table-2018

Every purchase price splits into two parts: the bank loan and your downpayment.

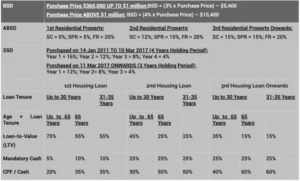

In Singapore, the maximum LTV for a first home loan (tenure under 30 years, borrower under 65) is 75%. That leaves a minimum downpayment of 25%, split between 5% cash and the rest from cash or CPF.

Push the loan tenure past 65, or stretch it beyond 30 years, and LTV drops to 55%. Already servicing another mortgage? Same 55% cap applies.

Downpayment is just the start. BSD, ABSD, legal fees, and (occasionally) agent commission all stack on top, and together they’re what you actually need in the bank before collecting your keys.

Purchase Price

BSD Rate

First $180,000

1%

Next $180,000

2%

Next $640,000

3%

Remaining amount

4%

Rough shortcut: under $1 million, BSD is about (Price × 3%) − $5,400. Above $1 million, it’s about (Price × 4%) − $15,400.

ABSD depends on residency and how many properties you already hold.

Buyer Profile

1st Property

2nd Property

3rd+ Property

Singapore Citizen

0%

20%

30%

Singapore PR

5%

30%

36%

Foreigner

60%

60%

60%

If ABSD applies to you, look into the legal ways to reduce it before you commit. It’s often the single biggest line item in the entire budget, bigger than legal fees and agent commission combined.

3. TDSR and MSR: Will the Bank Even Say Yes?

This is the one most first-timers skip. It’s also the one that kills deals at the worst possible moment.

Total Debt Servicing Ratio caps all your monthly debt, including the new mortgage, at 55% of gross monthly income. Buying an HDB flat? Mortgage Servicing Ratio applies too, capping housing repayments at 30% of income.

A $1,000,000 condo renting at $3,500 a month works out to ($3,500 × 12) ÷ $1,000,000 × 100 = 4.2%.

It’s a blunt tool. Most decent luxury condos for sale in Singapore sit somewhere between 2.5% and 4% gross yield, so anything well above that range deserves a second look at why.

6. Net Rental Yield (Cap Rate)

Net rental yield, or cap rate if you want the technical name, takes gross yield and strips out the real running costs. Property tax, maintenance, insurance, commission, all of it.

Formula: Net Rental Yield = (Net Rental Income ÷ Purchase Price) × 100

This is the number serious buyers trust. Gross yield can make a property look great right up until the maintenance bill shows up.

7. The 1% Rule

Borrowed from US property investing, but still a decent quick screen here. Monthly rent should be at least 1% of the purchase price for a unit to earn a closer look as a rental play.

On a $1,000,000 condo, that’s $10,000 a month in rent.

Very few Singapore condos actually clear a full 1% today. Prices have run well ahead of rents in most prime areas. Treat it as a screening tool, not gospel. Anything near or above 1% deserves priority attention. Anything under 0.5% needs a much stronger appreciation story to justify the price tag.

8. Gross Rent Multiplier (GRM)

GRM tells you roughly how many years of rent it would take to “buy back” the property, purely based on rental income.

Formula: GRM = Purchase Price ÷ Annual Rental Income

On that same $1,000,000 condo earning $42,000 a year in rent, GRM = $1,000,000 ÷ $42,000 = 23.8.

Lower GRM generally means better rental value. It’s one of the simpler real estate investment calculations on this list, and a fast way to rank a shortlist before digging deeper.

9. Debt Service Coverage Ratio (DSCR)

DSCR checks whether the rental income actually covers the mortgage repayment, which matters a lot more once interest rates move against you.

Formula: DSCR = Net Rental Income ÷ Annual Mortgage Repayment

A DSCR above 1.0 means rent covers the loan. Below 1.0, you’re topping up the shortfall from your own pocket every month. Most banks and seasoned investors like to see DSCR comfortably above 1.2, since that buffer absorbs a vacancy month or a rate hike without turning into a crisis. Of all the real estate investment calculations here, this is the one that quietly protects you when the market turns.

10. Cash-on-Cash Return

Cash-on-cash return measures cash flow against the actual cash you put in, not the full purchase price. Arguably more honest than gross yield, since it accounts for leverage.

Formula: Cash-on-Cash Return = (Annual Net Cash Flow ÷ Total Cash Invested) × 100

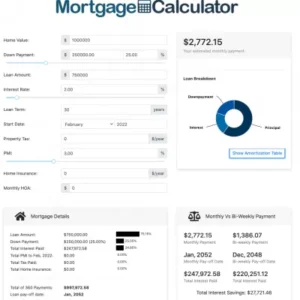

Take Peter and Jane. They buy a $1,000,000 condo with a $250,000 downpayment. Total cash outlay, downpayment plus closing costs, comes to $397,000. The unit rents for $3,500 a month, or $42,000 a year.

Cash-on-Cash Return = $23,520 ÷ $397,000 = 5.9%

If cash flow matters more to you than paper gains, this is the number to watch. It tells you how hard your money, not the bank’s, is actually working.

11. Payback Period

Payback period is how long it takes to recover your initial investment purely through rental income.

Formula: Payback Period = Purchase Price ÷ Annual Rental Income

Same $1,000,000 condo at $3,500 monthly rent: $1,000,000 ÷ $42,000 = 23.8 years.

Shorter is generally better, but a long payback period isn’t automatically a dealbreaker. Plenty of prime district units carry long payback periods because buyers are paying for appreciation and prestige over pure yield. Just know the number before you sign, not three years after.

12. Capital Appreciation

Nobody can predict this one with real precision, and anyone who tells you otherwise is selling something. Singapore private property has appreciated anywhere from 2% to over 16% in a given stretch, depending entirely on where you are in the cycle.

For planning purposes, model conservatively. Somewhere around 2.5% to 3% a year is a safer assumption than extrapolating off the best years the market has ever had.

A $1,000,000 property appreciating 3% a year for 5 years generates roughly $100,000 in paper profit. Against a $250,000 downpayment, that’s a 40% return on equity over 5 years, around 8% annually once leverage is factored in. That’s a genuinely solid figure.

13. Price Per Square Foot

The simplest tool in the whole toolkit, and still one of the most misused. PSF lets you compare units of different sizes on equal footing, whether within one development or across projects in the same district.

Formula: Price Per Square Foot = Purchase Price ÷ Floor Area (sq ft)

Don’t use PSF alone though. A lower PSF sitting next to a higher one in the same project usually points to a worse layout, a lower floor, or an awkward facing, not a bargain. Pair it with layout efficiency before drawing any conclusions.

Putting the Numbers Together

None of these real estate investment calculations mean much on their own. A property with a fantastic gross yield but a 40-year payback period and negative cash-on-cash return isn’t a good investment. It’s a trap wearing one flattering number as a disguise.

Here’s roughly how we sequence it for buyers we work with:

Check TDSR and MSR first, so your real budget is set before you view anything.

Work out total upfront cash outlay, including ABSD, so nothing surprises you at OTP stage.

Run gross and net rental yield to build a shortlist.

Apply the 1% rule and GRM as quick screens if rental income matters to you.

Check DSCR, cash-on-cash return, and payback period on your top two or three picks.

Model capital appreciation conservatively as the final gut check.

Do this properly and you walk into a purchase with your eyes open, instead of discovering three years in that the “great deal” barely broke even.

Getting the Numbers Right Before You Buy

You can run these calculations yourself, no question. But cross-checking them against current cooling measures, TDSR limits, and the specific development you’re eyeing takes local, up-to-date knowledge, and that’s really where a second pair of eyes helps.

If you’d like someone to run these numbers against your actual budget before you view a single unit, our team offers a straightforwardproperty consultation covering your TDSR, target yield, and holding strategy. For buyers thinking longer-term about entry timing, unit selection, and exit strategy, it’s worth a conversation with a dedicatedSingapore property investment advisor before making an offer.

At SG Luxury Condo, we’ve sat through enough of these conversations to know the buyers who do well aren’t the ones who moved fastest. They’re the ones who ran the real estate investment calculations first. If you’re browsingluxury condos for sale in Singapore and want someone to check your math before you commit, we’re happy to help.

Advanced Heading

Frequently Asked Questions

What is the most important real estate investment calculation?

There isn’t one single answer. Net rental yield shows the real return, cash-on-cash return shows how your own money is performing, and TDSR tells you whether the bank will even approve the loan. Skip any of them and you’re working off half the picture.

Is a high rental yield always a good sign?

Not always. Very high gross yields sometimes come attached to older buildings, weaker locations, or higher vacancy risk. Check net yield and the building’s condition before trusting a headline number.

How accurate is capital appreciation as a calculation?

It’s an estimate, not a promise. Use conservative assumptions and stay skeptical of anything projecting above 4-5% a year, no matter how good the sales pitch sounds.

What's a good cash-on-cash return in Singapore?

Anywhere from 4% to 6% is considered reasonable for a leveraged residential purchase here, given how tight yields are relative to prices. Anything higher usually comes with more risk attached somewhere.

Do I need to calculate DSCR if I'm not renting the unit out?

No. DSCR only matters for investment properties where rental income is meant to cover the mortgage. If you’re buying to live in it, TDSR is the number that matters instead.

What's the difference between gross yield and cap rate?

Gross yield ignores expenses. Cap rate (net yield) subtracts them. They can tell very different stories about the same property, which is why relying on gross yield alone is a common mistake.

How is ABSD calculated if I'm buying with my spouse?

ABSD is based on the profile of the buyer with the higher liability, and the number of properties either party already owns. It’s worth getting this checked before the OTP is signed, since it’s not always straightforward.

Should I use the 1% rule for Singapore condos?

Use it as a screen, not a hard filter. Very few units in prime or city-fringe locations will actually hit 1% today. It’s more useful for flagging units worth deeper investigation than for ruling properties out entirely.

What happens if my TDSR is too high?

The bank will reduce your loan quantum, or reject the application outright. Some buyers restructure existing debt, extend loan tenure, or bring in a co-borrower to bring TDSR back under 55%.

Can I do all these real estate investment calculations myself?

Yes, the math itself isn’t hard. What’s harder is knowing which numbers apply to your specific situation, especially around ABSD, TDSR, and current cooling measures, which is where a second opinion tends to pay for itself.

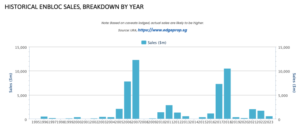

TL;DR: Buying a property mainly for its en bloc potential in Singapore is a gamble dressed up as a strategy. In 2025, only two residential en bloc sales went through, Chiku Mansions and River Valley Apartments, both freehold and over 40 years old. Most attempts fail, the process can drag on for years, and you’re left holding an ageing asset with rising maintenance costs and a thinner sinking fund the whole time you wait. If the en bloc happens, great. If it doesn’t, and statistically it usually doesn’t, you’re stuck with a property that was never really the point.

Someone will always tell you the story. A friend of a friend bought an old condo in the 2010s, barely thought about it for years, and then one day got a call saying the whole estate is going en bloc. Suddenly they’re sitting on a payout worth double what they paid. Tulip Garden’s 2018 sale is the one everyone still brings up, some owners walked away with $4.3 million to $7.6 million per unit.

Stories like that are why “en bloc potential” gets thrown around so casually by agents showing older units. But here at SG Luxury Condo, we’ve sat across the table from enough buyers who bought purely chasing that dream to know it rarely plays out the way the story goes. This is an update to our earlier piece on the topic, with the latest numbers on en bloc potential in Singapore and what’s actually changed heading into 2026.

What “En Bloc Potential” Actually Means

An en bloc, or collective sale, happens when the majority of owners in a condo agree to sell the whole development to one buyer, almost always a property developer. The developer tears it down and builds something new, usually with more units, thanks to unused plot ratio the old low-rise building never took advantage of.

For a sale to go through, owners need to hit a consent threshold. Right now that’s 80% for developments 10 years or older, and 90% for anything younger, measured by both strata share value and floor area at the same time. This is being reviewed in 2026, and there’s real discussion about lowering that threshold, so it’s worth keeping an eye on if you’re weighing this decision.

When agents say a unit has “en bloc potential,” they usually mean the building sits on a large freehold or 999-year leasehold plot, has a low plot ratio compared to what the URA Master Plan now allows, and is old enough that maintenance costs are starting to bite. On paper, that sounds like a smart, patient investment. In practice, it’s a lot messier.

The Real Pitfalls of Buying a Property for En Bloc Potential

Let’s go through what actually goes wrong, because the risks here are bigger than most buyers realize going in.

It Might Never Happen

This is the big one. In the whole of 2025, only two residential en bloc sales closed in Singapore, Chiku Mansions and River Valley Apartments. Both were freehold, both over 40 years old. Out of hundreds of ageing condos across the island, two crossed the finish line. That’s the actual base rate you’re betting against, not the Tulip Garden story from 2018.

Developers now have an easier path anyway. The government has been ramping up Government Land Sales, giving developers cleaner, faster land without needing to negotiate with hundreds of individual owners. Why would a developer go through years of committee meetings and legal objections when a GLS tender gets them land in months?

The Timeline Is Brutally Long and Uncertain

Even when an en bloc does go somewhere, the process from forming a Collective Sale Committee to actual completion typically takes two to five years. The Collective Sale Agreement itself is only valid for twelve months, so if owners can’t agree on a price or find a buyer in time, the whole thing can collapse and owners have to start over from scratch.

If you’re buying with en bloc potential as your main reason, you need to be genuinely fine with your money sitting there for five, ten, even fifteen years with zero guarantee of a payout at the end.

Ageing Buildings Come With Real, Ongoing Costs

Here’s the part a lot of buyers overlook. While you’re waiting for an en bloc that may or may not happen, you’re still living in, or paying maintenance on, an ageing building. Condos over 30 years old typically need electrical rewiring, plumbing replacement, lift overhauls, and pool refurbishment, all of which cost real money.

Before buying into any older development for its en bloc potential, always ask for the MCST’s audited financial statements. A thin sinking fund means a special levy bill could land on your doorstep on top of your mortgage, regardless of whether the collective sale ever materializes.

You’re Often Paying an “En Bloc Premium” Already

The moment a development becomes known as a potential en bloc candidate, buyers start paying above its actual market value just for the hope attached to it. That premium reflects speculation, not the value of the home itself. If the en bloc falls through, and it usually does, you’ve overpaid for a unit that might now be harder to resell, since the next buyer will ask the same questions you should have.

Minority Owners Can Block or Delay the Sale

Singapore’s collective sale laws exist specifically to protect owners who don’t want to sell. Anyone who doesn’t sign the Collective Sale Agreement can object to the Strata Titles Board once the application is submitted, citing an unfair price, an inequitable distribution formula, or a lack of good faith in the process. Corporate unit owners are another wrinkle buyers rarely think about, they sometimes have different incentives than individual owner-occupiers and can slow negotiations considerably.

Higher Developer ABSD Has Cooled the Whole Market

Developer Additional Buyer’s Stamp Duty currently sits at 35%, with a conditional remission of 30% if the developer completes construction and sells every single unit within five years of the collective sale. That’s a tight, risky window, especially for large mega-sites with 800 or more units. It’s a big reason developers are now chasing smaller, boutique sites under $100 million with 50 to 100 units instead of the sprawling estates that dominated the 2017 to 2018 boom.

If your building is a large multi-block estate, this ABSD structure alone makes a successful en bloc materially less likely than it would have been a decade ago.

You Might Face Seller’s Stamp Duty If It Actually Happens Too Soon

Ironically, if the en bloc does succeed but happens shortly after you bought your unit, you could get hit with Seller’s Stamp Duty. For residential property bought on or after 4 July 2025, the SSD holding period is four years, and the rate starts at 16% if you’ve held the unit for less than a year, stepping down by four percentage points each additional year. Buy in hoping for a quick payout and you might end up handing a chunk of it straight back. We’ve broken down how stamp duty costs stack up for different buyer profiles in our guide onhow to avoid overpaying on ABSD, which is worth a read alongside this one since the two costs often show up together in the same transaction.

En Bloc Success vs Failure: A Quick Snapshot

Factor

Higher Success Odds

Lower Success Odds

Tenure

Freehold or 999-year leasehold

99-year leasehold with long lease remaining

Building age

20 to 40+ years

Under 15 years

Development size

Boutique, under 200 units

Mega estate, 800+ units

Plot ratio

Significant uplift potential under URA Master Plan

Already built to max plot ratio

Location

CCR or RCR, near upcoming MRT or rezoning

Suburban with limited redevelopment upside

Owner sentiment

Aligned owner base, low maintenance fund concerns

Fragmented ownership, corporate holdouts

Even developments that check every box on the “higher odds” side still fail more often than they succeed. That table tells you what improves your chances, not what guarantees an outcome. It’s the exact framework SG Luxury Condo uses when we’re asked to assess a specific building’s en bloc odds for a client.

So Should You Ever Buy With En Bloc Potential in Mind?

Not as your main reason, no. If you’re buying an older, well-located freehold condo because you genuinely like living there, the price is fair on its own merits, and the building is well maintained, then a possible en bloc down the road is a nice bonus you might never see. That’s a very different mindset than buying a tired 40-year-old unit purely because an agent mentioned “en bloc potential” three times during the viewing.

At SG Luxury Condo, our honest advice is this. Buy the property because it makes sense today, the location, the layout, the price per square foot compared to similar resale units nearby. Treat any future en bloc as a lottery ticket that came free with the purchase, not the reason you bought it. We’ve written a deeper breakdown of these risks, including real 2024 and 2025 case data, in our guide onthe real dangers of buying an en bloc property in Singapore, worth a read if you’re seriously weighing this route.

If you’re an HDB upgrader stepping into private property for the first time, this decision matters even more, since your capital is likely more limited and less able to absorb years of uncertainty. Talking it through with aSingapore property investment advisor before you commit can save you from a decision you’re locked into for a decade. Ourproperty agents in Singapore can also pull the actual transaction and en bloc history for any specific building you’re eyeing, rather than relying on what a listing agent tells you.

What to Check Before You Buy an Older Condo “For En Bloc Potential”

If you’re still considering it, at least go in with your eyes open. Here’s what SG Luxury Condo tells every client to actually verify before signing anything.

Request the MCST’s latest audited financial statements and sinking fund balance

Check the building’s plot ratio against current URA Master Plan allowances for that district

Find out the tenure, freehold and 999-year leasehold sites are far more attractive to developers than 99-year leasehold

Look at how fragmented ownership is, smaller unit counts generally reach consensus faster

Ask whether any past en bloc attempts failed and why, repeat failures are a red flag, not a sign it’s “due”

Factor in five to fifteen years of holding costs, maintenance, and opportunity cost if the sale never happens

A Word From SG Luxury Condo

We’ve walked plenty of clients through this exact decision, and the pattern is always the same. The buyers who end up happy are the ones who bought a home they actually wanted to live in or rent out, where any future en bloc potential was simply icing on the cake. The buyers who end up frustrated are the ones who bought purely on the promise of a payout that, statistically, almost never comes.

If you’re weighing an older resale unit against a newer launch and want an honest read on the numbers rather than a sales pitch, our team at SG Luxury Condo is happy to walk through it with you. You can also browse our full range ofluxury condos for sale in Singapore if you’d rather skip the guesswork entirely and go with something that stands on its own value today.

Advanced Heading

Frequently Asked Questions

What does "en bloc potential" actually mean when an agent mentions it?

It usually means the building sits on a large freehold or 999-year leasehold plot with a low plot ratio, meaning a developer could build significantly more units if the site were redeveloped. It’s a possibility, not a promise.

How common are successful en bloc sales in Singapore right now?

Not very. In 2025, only two residential collective sales completed islandwide, Chiku Mansions and River Valley Apartments. Compare that to the 2017-2018 peak, when over 30 sales closed in a single year.

Is it worth paying more for a unit just because it has en bloc potential?

Generally, no. That extra “en bloc premium” reflects speculation, not the home’s actual value. If the sale doesn’t happen, you’ve simply overpaid for a property that may be harder to resell later.

How long does an en bloc sale usually take from start to finish?

Typically two to five years from the formation of the Collective Sale Committee to actual completion, and that’s assuming it succeeds at all. The Collective Sale Agreement itself is only valid for twelve months before it needs to be renewed.

Can a minority of owners block an en bloc sale?

Not entirely, but they can object to the Strata Titles Board, and if the board finds the sale unfair or conducted in bad faith, it can be delayed or rejected. Owners who don’t sign the Collective Sale Agreement do have real legal recourse.

Why has en bloc activity slowed down so much since 2018?

A big reason is developer ABSD, currently 35% with a conditional 30% remission if the developer completes and sells out within five years. That tight window makes large estates riskier to bid on, so developers increasingly prefer smaller, boutique sites or straightforward Government Land Sales tenders instead.

Do freehold condos have better en bloc chances than leasehold ones?

Yes, generally. Freehold and 999-year leasehold sites are far more attractive to developers since there’s no lease decay to worry about after redevelopment. Most successful en bloc sales in recent years, including both 2025 completions, were freehold developments.

What happens to my money if I buy expecting an en bloc and it never happens?

You’re left owning an ageing property with mounting maintenance needs and possibly a thinner sinking fund than when you bought it. Your capital stays tied up in that asset, and you’ve likely paid a premium for potential that never materialized.

Could I get hit with extra stamp duty if the en bloc happens shortly after I buy?

Possibly. For residential property bought on or after 4 July 2025, Seller’s Stamp Duty applies if the sale happens within four years, starting at 16% for the first year and stepping down after that. A fast en bloc payout could mean handing a chunk of it back.

Is the en bloc consent threshold likely to change soon?

It’s currently under review in 2026, with discussion around lowering the threshold below the current 80% and 90% marks. If that happens, it could make future collective sales somewhat easier to push through, though nothing has been finalized yet.

TL;DR: Right now, ParkTown Residences, Skye at Holland, The Orie, Springleaf Residence, and Rivelle Tampines EC are the standout best selling condos in Singapore, most of them crossing 90%+ sold within months. What they share is simple: good MRT access, fair launch pricing, and real scarcity in that specific pocket of town. Fast sales are a good signal, but they’re not the whole story. Keep reading and we’ll get into why.

Every few months someone asks us the same thing at SG Luxury Condo: “which condo is everyone buying right now?” Fair question, honestly. When a project sells out fast, it usually means buyers are seeing something in it worth paying for, whether that’s the location, the entry price, or just the fact that there’s nothing else like it nearby.

So instead of guessing or repeating the same old marketing lines, we went and pulled the real sales numbers. Here’s an honest look at the best selling condos in Singapore based on what’s actually happened at recent launches, not what a developer’s brochure claims.

Why “Best Selling” Actually Matters

A lot of people hear “best selling” and think it’s just a sales pitch. It isn’t, or at least it shouldn’t be treated that way. When a condo moves 80% or 90% of its units within launch weekend, that’s the market voting with real cash. Buyers aren’t guessing here. They’re comparing that project against everything else on the table and still picking it.

That’s why we keep such a close eye on this at SG Luxury Condo. If you want to know where demand is really heading in Singapore’s property market, the best selling condos usually give you a clearer picture than any analyst forecast will. It’s one of the main reasons clients come back to SG Luxury Condo before they commit to anything.

The Best Selling Condos in Singapore Right Now

Based on 2025 through early 2026 launch data, here’s what’s genuinely been flying off the shelf.

Project

District

Units

Take-up Rate

Why It Sold

ParkTown Residences

Tampines North

1,193

93% sold

Only mega launch of 2025, mixed-use with mall and MRT integration

Skye at Holland

Holland

666

99% sold

Rare Holland Village site, strong school belt appeal

LyndenWoods

Science Park Drive

343

94.5% sold

Sustainability-focused design, tech and research hub proximity

The Orie

Toa Payoh

777

86% sold at launch, 94% to date

First new private launch in Toa Payoh in over a decade

Springleaf Residence

Springleaf

941

96% sold

Walking distance to Springleaf MRT, forest-fringe location

Lentor Central Residences

Lentor

477

Fully sold

Part of the fast-growing Lentor precinct

The Continuum

District 15

816

82% sold to date

Freehold, District 1/2 alternative pricing

Rivelle Tampines (EC)

Tampines

572

Fully sold in a month

Rare EC launch, strong HDB upgrader demand

Line these up side by side and a pattern starts to show. None of this is luck. It’s the same handful of factors showing up again and again, and it’s exactly what SG Luxury Condo looks at with clients trying to spot the next best selling condo in Singapore before everyone else catches on.

What These Best Selling Condos Have in Common

Here’s what stood out once we actually dug into the numbers instead of just skimming headlines.

MRT connectivity isn’t optional anymore. Nearly every project on this list sits a short walk from a station. Buyers just won’t budge on this these days.

Scarcity sells. Skye at Holland moved quickly partly because Holland Village hasn’t had a new launch in years. Same story really with The Orie in Toa Payoh.

Pricing at launch matters more than people admit. Developers who price close to nearby resale stock tend to see faster take-up. Overpriced launches just sit there, no matter how good the showflat looks.

Mixed-use projects have an edge. ParkTown Residences did so well partly because it’s not only a condo. It’s a mall, a transport hub, and a neighbourhood centre in one package.

ECs are having a real moment. Rivelle Tampines sold out in under a month. HDB upgraders are clearly still chasing value, especially before the newer EC rules stretched out the privatisation timeline.

Best Selling Doesn’t Always Mean Best Investment

This is the bit a lot of guides skip over, and honestly it’s the most important part. A best selling condo in Singapore tells you what buyers wanted at launch. It doesn’t automatically tell you what will perform best over the next ten years. Some projects sell fast because they’re genuinely undervalued. Others sell fast because of a tight preview window, sharp marketing, or a bit of FOMO that doesn’t always hold once the crowd calms down.

At SG Luxury Condo, we tell clients the same thing every time. Look past the take-up rate. Ask why it sold fast. Was it the psf compared to resale units nearby? The schools within a kilometre? The MRT line? Once you actually understand the “why,” you can judge whether that same logic still holds up when you’re ready to sell in five or ten years.

If you’re weighing a new launch against something already built, talking to aSingapore property investment advisor before you commit can save you from paying a premium for hype you didn’t need to chase in the first place.

How to Spot the Next Best Selling Condo Before It Launches

You don’t need insider info to get ahead of the crowd here. A few things tend to repeat themselves.

Check the URA Master Plan for the area. New MRT lines or commercial rezoning almost always push demand up later.

Compare the land price (psf ppr) the developer paid against nearby recent launches. A cheaper land cost usually leaves room for a more competitive launch price.

Look at how many competing launches are scheduled nearby that same year. Less competition means a better shot at a fast sellout.

Pay attention to school proximity within 1km. It drives owner-occupier demand and, longer term, resale value too.

Watch first-weekend take-up rates closely. Anything above 80% is usually a sign the project will be fully sold within a few months.

We track all of this at SG Luxury Condo for every upcoming launch, so clients don’t have to sit and read through URA reports on their own. If you’d rather have someone walk you through which projects are actually worth queuing up for, ourproperty agents in Singapore can get you access to previews before the general public even hears about it.

Honestly, it depends on why you’re buying. If it’s for your own stay and the unit fits your budget and lifestyle, don’t overthink the sales numbers too much. But if you’re buying to invest, the best selling condos in Singapore right now are worth studying even if you never buy into that exact project. They show you where demand is piling up, which districts are heating up, and which price points still feel reachable to the average upgrader.

For a wider look at how project pricing tends to move after launch, our guide onluxury condo investments in Singapore covers how early buyers in past hot sellers actually did once the dust settled.

New Launch vs Resale: Which One Actually Makes More Sense Right Now

This question comes up in almost every conversation we have with buyers, and there’s no single right answer. It really depends on what you’re after.

Buying at launch, like grabbing an early unit at The Orie or Springleaf Residence before it sold out, usually gets you a lower entry price and first pick of the best stacks. You’re paying today’s price for a home that won’t be ready for another three or four years. That’s fine if you’re patient and don’t need to move in soon. It’s a lot less fine if you’re renting elsewhere and watching that cost pile up while you wait.

Resale works differently. You walk in, see exactly what you’re getting, and move in within a couple of months. The catch is you’re often paying a premium if the project already built a reputation, and older units might need some renovation work that new launches don’t. A resale unit at a project that already proved itself as one of the best selling condos in Singapore, say something like The Continuum a couple of years after launch, can actually be a smart middle ground. You get the track record without the multi-year wait.

Here’s a rough way to think about it. If your budget is tight and you can afford to wait, new launch usually stretches your dollar further. If timing matters more than price, or you want to see the actual unit and building before committing, resale tends to make more sense.

Rental Yield by District: Where Investors Are Actually Getting Returns

Take-up rate tells you how fast a condo sold. It doesn’t tell you what kind of rent you’ll actually collect once it’s built, and that’s the part a lot of buyers overlook until they’re already holding the keys.

Broadly speaking, prime districts like Orchard, River Valley, and the rest of the Core Central Region tend to sit around 2% to 3% gross rental yield. You’re paying a premium for the address and the tenant pool skews toward expats and executives who can afford it, but the yield itself is usually the lowest across the island simply because purchase prices are so high to begin with.

Outside the central region, districts like Tampines, Sengkang, and other OCR pockets typically run higher, somewhere around 3% to 4.5%. Lower entry prices mean your rent as a percentage of what you paid looks a lot better on paper, even if the actual dollar amount is smaller than what a Core Central unit might fetch.

A few districts worth watching if yield is your main goal:

Tampines and the East – strong tenant demand from the regional business hub and Changi-related jobs, plus decent MRT coverage

Toa Payoh and the central fringe – close enough to the CBD to attract tenants who don’t want to pay CCR rent, without the CCR price tag

Lentor and the North – newer precinct, still building up its tenant base, but early numbers look promising given the MRT access

If rental income is the main reason you’re buying, it’s worth running the yield math before you fall for a unit just because it’s on our best selling condos list. A project that sold out fast at launch isn’t automatically the one that’ll rent out fastest or fetch the strongest yield down the line. Those are two different questions, and it’s easy to mix them up.

A Quick Word From SG Luxury Condo

We’ve been tracking Singapore’s best selling condos for years now, and one thing hasn’t really changed. The projects that sell fast at launch almost always share the same three or four traits: good connectivity, fair pricing, and genuine scarcity in that specific spot. Everything else is just noise around it.

If you’re comparing a few shortlisted projects and want a second opinion before you commit, that’s exactly the kind of call SG Luxury Condo helps clients work through every week. Whether you’re chasing the next best selling condo Singapore has to offer or you’d rather browse the full range ofluxury condos for sale in Singapore, our team can talk you through what’s actually worth your money, not just what happens to be trending this month.

Advanced Heading

Frequently Asked Questions

What makes a condo a "best selling" project in Singapore?

Mostly it comes down to the take-up rate, meaning how many units sold during the launch weekend or within the first few months after. A project crossing 80% sold on launch day is generally seen as a best selling condo in Singapore.

Are best selling condos always the best investment?

Not always, no. Fast sales show strong day-one demand, but long-term performance comes down to things like future supply nearby, rental demand, and whether the launch price already baked in most of the upside.

Which district has the most best selling condos right now?

It shifts year to year depending on supply. At the moment, Tampines, Toa Payoh, and the Lentor precinct have all had standout launches, mostly thanks to MRT connectivity and a shortage of new supply in those pockets.

Should I buy an EC if it's selling fast?

Depends on your eligibility and your plans. ECs like Rivelle Tampines sell quickly because of the price gap versus private condos, but the newer EC rules stretch out the minimum occupation period before you can sell or fully privatise, so factor that into your timeline.

How do I find out about upcoming best selling condos before they launch?

The simplest way is to work with an agent who has direct developer relationships and gets early access to previews. SG Luxury Condo tracks upcoming Government Land Sale sites and new launches months in advance, so clients get first pick before public balloting even opens.

Does a high take-up rate mean the price will keep going up after launch?

Not necessarily. A fast sellout tells you demand was strong on day one, but resale price growth depends on what happens in the surrounding area afterward, new MRT lines, nearby launches, rental demand, that kind of thing. Some best selling condos do go on to see solid appreciation. Others plateau once the initial excitement fades.

Why do some best selling condos still have units left months after launch?

Even a strong sellout rarely means every single unit moves on day one. Larger or oddly configured units, like penthouses or ground floor units facing a busy road, often take longer to sell even at popular projects. That’s usually not a red flag, it’s just normal for bigger developments with hundreds of units and a wide unit mix.

Is it better to buy at launch or wait for a resale unit in a best selling condo?

Both have upsides. Buying at launch usually means a lower entry price and first pick of the best stacks, but you’ll wait a few years for TOP. Resale units in an already popular project let you move in sooner and skip the wait, though you’ll likely pay a premium if the project has already seen strong appreciation.

Do best selling condos always have the highest rental demand?

Often, but not always. A condo that sold fast because of great connectivity or a rare freehold tenure will usually rent well too, since those same factors matter to tenants. That said, rental demand also depends on nearby office clusters, expat pockets, and school catchments, so it’s worth checking those separately rather than assuming a fast sellout guarantees strong rental yield.

Can foreigners buy into these best selling condos the same way locals can?

Yes, foreigners can buy private condos in Singapore, including best selling launches, without special approval. The main difference is the Additional Buyer’s Stamp Duty, which sits at 60% for foreign buyers, so it’s worth running your numbers properly before you join a launch queue.

TL;DR: Yes, foreigners can buying property in Singapore; no special approval needed. Landed houses and HDB flats are mostly off limits. The catch is the 60% Additional Buyer’s Stamp Duty on top of the purchase price, plus regular Buyer’s Stamp Duty. Banks will still give you a mortgage, just expect a lower loan amount and a bit more paperwork. Talk to a local agent before you fall in love with a unit, it’ll save you money and stress.

If you’ve been eyeing a home in Singapore and typing “can foreigners buying property in Singapore” into Google at midnight, you’re not alone. It’s one of the first questions almost every overseas buyer asks us at SG Luxury Condo, usually right after “which neighbourhood should I even be looking at?”

The good news is that the answer isn’t complicated once someone walks you through it properly. The confusing part is that most of what’s online mixes up rules for citizens, Permanent Residents, and foreigners, and doesn’t tell you what it actually costs to buy as a non-resident. So let’s clear that up here, in plain English, without the legal jargon.

The Short Answer: Yes, Foreigners Buying Property in Singapore

Foreigners are allowed to buy private condominiums and apartments in Singapore without needing any special government approval. This has been the case for years and hasn’t changed. What you can’t do freely is buy landed houses (think terrace houses, bungalows, semi-detached homes) or HDB flats, which are Singapore’s public housing. Those come with restrictions that make them impractical for most overseas buyers anyway.

So if your plan is a condo, and for most foreign buyers it is, you’re in good shape. This is actually one reason why luxury condos for sale in Singapore have become such a popular entry point for foreign investors and expats. It’s the one property category where ownership is genuinely straightforward.

What Foreigners Can and Can’t Buy: The Breakdown

Here’s how it actually splits, based on Singapore’s Residential Property Act.

You can buy without approval:

Private condominiums and apartments (any size, any launch)

Executive condominiums, but only once they’re more than 10 years old

Strata landed homes within approved condo developments, like some units in Sentosa Cove

Leasehold landed property with a lease of 7 years or less

You’ll need approval from the Singapore Land Authority (SLA):

Landed houses such as bungalows, terrace houses, and semi-detached homes on the mainland

Vacant residential land

You generally can’t buy at all:

HDB flats, unless you’re married to a Singapore citizen and meet other conditions

Good Class Bungalows (GCBs), except under very rare circumstances tied to significant economic contribution

Sentosa is the one exception worth knowing. It’s the only part of Singapore where foreigners can buy landed homes without prior SLA approval, which is part of why Sentosa Cove bungalows attract so much overseas interest.

The Real Cost: ABSD and Stamp Duty for Foreign Buying property in Singapore

This is the part most people underestimate, and honestly, it’s the number that changes the whole conversation. On top of the price of the property, every buyer in Singapore pays Buyer’s Stamp Duty (BSD), and foreigners also pay Additional Buyer’s Stamp Duty (ABSD) on top of that.

Buyer Profile

ABSD Rate (2026)

Singapore Citizen, 1st property

0%

Singapore Citizen, 2nd property

20%

Permanent Resident, 1st property

5%

Permanent Resident, 2nd property

30%

Foreigner (non-PR)

60%

Nationals of the US, Switzerland, Liechtenstein, Norway, Iceland

0% (under free trade agreement terms)

Yes, 60% is a big number, and it applies regardless of how many properties you already own here. It’s the biggest single factor in your budget planning, and it’s exactly why we always recommend foreign buyers speak to a proper Singapore property investment advisor before they start browsing listings, not after they’ve already fallen in love with a unit. Getting the tax math right at the start saves a lot of headaches later.

A few nationalities get a break here. Buyers from the US, Switzerland, Liechtenstein, Norway, and Iceland pay the same rate as a Singapore citizen would, thanks to free trade agreements. Worth checking if you qualify before you assume the worst.

Buyer’s Stamp Duty is a smaller, tiered cost that everyone pays regardless of nationality, ranging from 1% to 6% depending on the purchase price. It’s not the deal-breaker ABSD can be, but it still needs to be in your budget.

Financing: Can Foreigners Get a Mortgage in Singapore?

Yes, and Singapore banks are generally quite comfortable lending to foreign buyers, though the terms are a bit tighter than what locals get. Here’s roughly what to expect:

Loan-to-value (LTV) ratio typically sits between 60% and 75%, meaning you’ll need 25% to 40% in cash or CPF (if applicable) upfront

Interest rates for foreigners can run slightly higher than for citizens or PRs

Banks will look closely at your income, employment stability, and existing debt obligations

ABSD and BSD must be paid fully in cash upfront, they can’t be financed through your home loan

If you’re not planning to finance and intend to pay in cash, this whole process moves a lot faster. Either way, it’s worth getting a mortgage in-principle approval before you start viewing units seriously, so you’re not negotiating on a property you can’t actually finance.

How the Buying Process Actually Works, Step by Step

Set your budget including ABSD, BSD, legal fees, and agent commission, not just the sticker price of the unit

Get pre-approved for financing if you’re taking a loan, so you know your real spending power

Shortlist properties with a property agent in Singapore who understands what foreign buyers can and can’t purchase, this avoids wasted time on ineligible listings

View units and negotiate the price and terms with the seller or developer

Pay the Option Fee (usually 1% to 5% of the price) to secure an Option to Purchase (OTP)

Exercise the option within the agreed period, typically 2 weeks, paying the balance deposit

Engage a conveyancing lawyer to handle the Sale and Purchase Agreement and title transfer

Complete the transaction, pay remaining stamp duties, and collect your keys

New launch purchases follow a slightly different, more regulated process through the developer, but the core idea is the same.

Where Foreigners Buying Property in Singapore

There’s no single “right” district, but certain areas come up again and again with our foreign clients. Orchard and River Valley remain popular for their central location and prestige. The Core Central Region attracts investors chasing capital appreciation and rental demand from expats. Sentosa Cove is the obvious pick for anyone specifically wanting a landed home by the water. And districts near good international schools, like Bukit Timah and Holland Village, tend to draw families relocating for work.

If you’re still weighing up whether Singapore property is the right investment for you at all, our piece onwhy foreigners are buying property in Singapore digs into the actual motivations we’re seeing on the ground, beyond just the tax numbers.

Is the 60% ABSD Worth It?

This is the honest question everyone eventually asks, and it deserves an honest answer. For some buyers, yes. Singapore’s political stability, strong currency, transparent legal system, and consistent long-term capital growth make it a market where the upfront cost can pay off over a 5 to 10 year horizon, especially with prime freehold condos that hold value well.

For others, particularly short-term speculators, the 60% ABSD makes the math much harder to justify. There are also legitimate ways to reduce your exposure depending on your structure and nationality, which is a conversation worth having with a specialist rather than guessing. If you want the mechanics spelled out, our guide onhow to avoid overpaying on ABSD walks through the legal options available to foreign buyers.

Final Thoughts

Buying property in Singapore as a foreigner isn’t complicated once you understand the rules, but it’s also not a market where guessing your way through it is a good idea. Between ABSD calculations, financing limits, and picking the right district and unit type, a lot of foreign buyers end up overpaying or missing better options simply because nobody walked them through it properly.

Advanced Heading

Frequently Asked Questions

Can Permanent Residents buy property in Singapore the same way as citizens?

Not quite. PRs are still classified as foreigners under the Residential Property Act, though they get a lower ABSD rate (5% on their first property) and more access to resale HDB flats after meeting a minimum residency period.

Do I need to be physically in Singapore to buy a condo?

No, but it makes the process smoother if you can visit at least once, or work with a trusted agent who can represent your interests locally.

Is there capital gains tax on property sales in Singapore?

No, Singapore doesn’t impose capital gains tax, which is one of the reasons the market remains attractive despite the ABSD.

Can I rent out my condo after buying it as a foreigner?

Yes, and many foreign owners do exactly this. Just note that short-term rentals under 3 months are not allowed for private residential property.

How much money do I actually need upfront to buy a condo as a foreigner?

More than most people expect, honestly. Between the cash downpayment (usually 25% to 40% if you’re financing), the 60% ABSD, and BSD, you’re looking at a big chunk of the purchase price in cash before the bank loan even kicks in. On a $2 million condo, that can easily mean over $1 million upfront. This is exactly why budgeting properly before you start viewing units matters so much.

Can I buy a Singapore property under a company or trust instead of my own name?

You can, and some foreign buyers do this for estate planning or tax reasons, but it doesn’t get you out of paying ABSD, it just changes how the transaction is structured. Get proper legal advice before going this route, since the paperwork and long-term implications are different from a straightforward personal purchase.

Do foreigners pay higher property tax every year compared to citizens?

Not really, the annual property tax rate is based on whether you live in the unit or rent it out, not your nationality. Owner-occupied homes get a lower rate, rented-out units get taxed a bit higher. Your passport doesn’t change that part.

Is buying new launch different from buying a resale condo as a foreigner?

The eligibility rules are the same either way. What changes is the process. New launches go through the developer directly with a fairly fixed timeline and payment schedule, while resale is a private negotiation between you and the seller, so there’s more room to haggle on price and terms.

What happens if I want to sell my Singapore condo later, are there extra fees for foreigners?

Selling itself works the same for everyone. You might owe Seller’s Stamp Duty if you sell within a few years of buying, but that applies to all owners, not just foreigners. And since Singapore has no capital gains tax, whatever profit you make on the sale isn’t taxed, which is a nice bonus.

Can my spouse and I both be on the title if only one of us is a foreigner?

Yes, joint ownership between a citizen or PR and a foreigner is allowed. Just know that the ABSD is usually calculated based on the higher applicable rate between the buyers, so it’s worth running the numbers with your agent before deciding how to structure the purchase.

Property AI

Here's a few ways we can help you

🤖

Would you like our AI Bot to help you find the perfect property? Our AI Bot can scrape through hundreds of property listings and provide you with a list of properties that matches your criteria.

Just now

⚡

🎯 Got it! AI is tailoring your feed...

What's happening now:

Scanning: Matching your criteria against 22,000+ active listings.

Analyzing: Filtering for your specific lifestyle preferences.

Curating: Picking the top 5 properties that hit every requirement.

⏳ We will analyze your search string. Real-time listings matching your exact lifestyle profile are loading and we will get back to you soon!