2025 URA Property Statistics: Private Home Demand Stays Resilient

Singapore’s private residential property market ended 2025 on a stable and confident note. According to the latest URA Real Estate Statistics for 4Q 2025, private home prices continued to rise, transaction volumes remained healthy, and buyer confidence carried through from the strong momentum seen in the third quarter.

While overall sales volumes moderated slightly due to fewer launches and the typical year-end slowdown, the underlying demand for private homes stayed intact. More importantly, the data points to a firm outlook heading into 2026, supported by controlled supply, stable economic conditions, and sustained owner-occupier demand.

For HDB upgraders, first-time private buyers, and long-term investors, the 4Q 2025 figures provide valuable insight into where the market stands today—and where it may be heading next.

Private Home Prices Continue a Steady Uptrend in 4Q 2025

In the fourth quarter of 2025, Singapore’s All-Residential Private Property Price Index rose by 0.6% quarter-on-quarter, extending the growth seen in the previous quarter. While this was slightly slower than the 0.9% increase in 3Q 2025, it still marked the fifth consecutive quarter of price growth, reinforcing the market’s underlying stability.

On a year-on-year basis, private home prices rose 3.3% in 2025, with much of the growth driven by the landed housing segment. This gradual pace of appreciation suggests that the market is expanding in a controlled and sustainable manner, rather than overheating.

For buyers who have been waiting on the sidelines, the data shows that prices are not retreating—but neither are they surging aggressively. This environment tends to favour decisive buyers who are financially ready, rather than those hoping for sharp price corrections.

Transaction Volumes Dip Seasonally, But Full-Year Activity Remains Strong

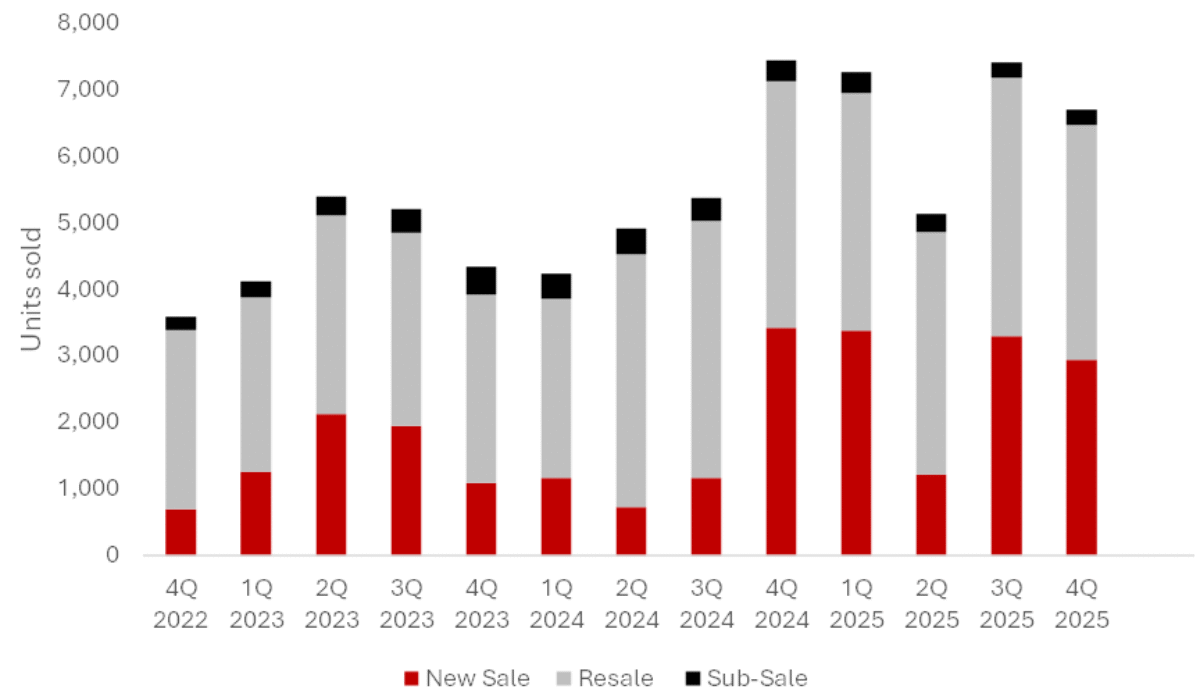

A total of 6,699 private home transactions were recorded in 4Q 2025, representing a 9.5% quarter-on-quarter decline. This moderation came after a very strong 3Q 2025, which saw heightened activity driven by eight major project launches.

The softer fourth-quarter performance was largely expected. Developers typically slow down launches toward the end of the year, and buyer activity often dips in December due to school holidays and year-end travel. Importantly, this was a seasonal slowdown rather than a demand-driven pullback.

For the full year, total private home sales reached 26,492 units, highlighting the resilience of Singapore’s housing market even amid global uncertainties earlier in the year.

New Home Sales Remain the Key Demand Driver

Despite fewer launches in 4Q 2025, the primary (new home) market remained robust. Developers sold 2,940 new private homes during the quarter, only a modest decline from the previous quarter’s strong showing.

Across the whole of 2025, 10,815 new homes were sold, making it the best-performing year since 2021. This reflects sustained confidence among buyers, particularly owner-occupiers who are less sensitive to short-term market fluctuations.

A key trend worth noting is the high take-up rates at launch. In 4Q 2025, four out of five new launches achieved over 80% sales on launch day. This mirrors the strong launch-day demand seen in 3Q 2025 and suggests that well-priced, well-located projects continue to attract immediate buyer interest.

For HDB upgraders, this highlights an important reality: desirable new launches do not stay available for long, especially when supply is limited.

Fewer Completions Are Pushing Buyers Toward New Launches

One structural factor shaping the market is the low number of private home completions. In 2025, only 6,123 private homes (excluding ECs) were completed, significantly lower than the 8,460 units completed in 2024.

This reduced completion pipeline has limited resale and sub-sale supply, pushing more buyers toward the new home market. As a result, developers with ready projects have benefited from spillover demand, especially in popular city-fringe and suburban locations.

This supply dynamic is expected to remain relevant in the near term, which helps explain why developers continue to enjoy strong sales momentum despite fewer launches.

Unsold Inventory Continues to Decline

Unsold private residential stock fell 5.2% quarter-on-quarter to 16,193 units in 4Q 2025. This decline came even after several new projects were launched, reflecting healthy absorption rates across the market.

Lower unsold inventory levels generally support price stability, as developers face less pressure to discount aggressively. It also reinforces the idea that demand is keeping pace with supply, particularly for projects that align well with buyer expectations around pricing, location, and layout.

Non-Landed vs Landed Homes: Diverging Price Performance

Non-Landed Homes See More Moderate Growth

Non-landed private homes recorded slower price growth in 4Q 2025, with prices edging down slightly after stronger gains in the previous quarter. This moderation was largely due to a smaller number of launches compared to 3Q 2025, when eight projects entered the market.

That said, price performance varied significantly by region.

Outside Central Region (OCR) non-landed homes saw the strongest growth, rising 1.0% quarter-on-quarter, supported by the strong performance of Faber Residence, which achieved over 90% sales during the quarter.

Rest of Central Region (RCR) prices rose 0.7% quarter-on-quarter, continuing the upward momentum from earlier launches such as Zyon Grand, Penrith, and The Sen.

Core Central Region (CCR) prices declined 3.5% quarter-on-quarter, ending four consecutive quarters of growth. This was largely due to lower transaction volumes, rather than weak interest, as pricing expectations between buyers and sellers temporarily diverged.

Landed Homes Outperform on the Back of Upgrader Demand

The landed housing segment was a standout performer in 4Q 2025. Prices rose 3.4% quarter-on-quarter, accelerating from the previous quarter and marking the fourth consecutive quarter of growth.

On a year-on-year basis, landed home prices climbed 7.7% in 2025, significantly outpacing non-landed homes. This trend reflects growing interest from condominium owners who were able to upgrade as their property values appreciated.

Transaction volumes for landed homes also increased, with 491 transactions in 4Q 2025, bringing the full-year total to 1,852 transactions, an 11.2% increase over 2024.

Demand was particularly resilient in the OCR and RCR, where buyers found a better balance between space, affordability, and location. In contrast, CCR landed transactions slowed as higher prices led to a temporary standoff between buyers and sellers.

Resale and Sub-Sale Markets Hold Steady

The resale private home market recorded 3,529 transactions in 4Q 2025, a slight moderation from the previous quarter. However, full-year resale transactions totalled 14,622 units, largely in line with 2024 levels.

This consistency highlights the resilience of the resale segment, even as it competes with attractive new launches and faces seasonal slowdowns.

Sub-sale activity remained muted, with only 230 transactions in 4Q 2025. The limited number of new completions in 2025 reduced opportunities for sub-sale transactions, a trend that is likely to persist until completion volumes rise again.

Rental Market Begins to Stabilise

After several years of strong rental growth, the private residential rental market showed signs of stabilisation in 4Q 2025. The All-Residential Rental Price Index dipped 0.5% quarter-on-quarter, reversing the modest increase seen in the previous quarter.

Non-landed rents declined marginally, while landed rents saw a steeper adjustment. Despite this short-term pullback, overall private rents still rose 1.9% for the full year, indicating that rental demand remains structurally supported.

Looking ahead, a growing supply pipeline—combined with policies such as the extended occupancy cap—is expected to keep rental growth in check through 2026 and 2027. For tenants, this could translate into more stable and negotiable rental conditions.

Upcoming Launches in 2026: Supply Remains Managed

The new launch pipeline in 2026 is shaping up to be active but controlled. The year began with the successful launch of Coastal Cabana EC, which sold more than two-thirds of its units shortly after launch.

For the full year, around 19 private residential projects comprising approximately 9,852 units, along with five EC developments offering nearly 2,000 units, are expected to enter the market. These projects span the CCR, RCR, and OCR, catering to a wide range of buyer profiles.

The continued release of land through the GLS programme reflects the government’s commitment to maintaining a stable housing supply and preventing excessive price volatility.

Market Outlook for 2026: Stability with Moderate Growth

The slight pullback in transactions during 4Q 2025 does not signal a weakening market. Instead, it reflects a natural pause following an exceptionally strong third quarter and the usual year-end slowdown.

Heading into 2026, Singapore’s private residential market is expected to remain resilient, supported by:

- Strong owner-occupier demand

- Limited unsold inventory

- Controlled supply from GLS sites

- Stable employment and income conditions

Barring unexpected global shocks, new home sales in 2026 are projected to range between 9,000 and 10,000 units, while resale transactions are expected to remain in the 13,000 to 14,000 range.

For buyers, this suggests a market that rewards preparation and decisiveness rather than speculation. Prices are likely to trend upward gradually, making well-timed purchases more important than trying to time a market bottom.

Final Thoughts: What This Means for Buyers and Upgraders

The 4Q 2025 URA statistics confirm that Singapore’s private property market remains fundamentally healthy. Demand has proven resilient, supply is being carefully managed, and price growth continues at a sustainable pace.

For HDB upgraders, the ongoing strength in both resale HDB prices and private home demand presents a window of opportunity to transition into private housing with confidence. For first-time private buyers, the coming year offers a diverse range of new launches across different regions and price points.

As always, the key lies in understanding your budget, timing your move strategically, and choosing projects that align with both lifestyle needs and long-term value.