From Investments to Keys in Hand: How Smart Investing Helps You Buy Your Dream Home in Singapore

From Investing to Homeownership: Turning Long-Term Plans Into Reality

Buying a home is one of life’s biggest financial milestones. For many Singaporeans, it marks independence, family growth, or a long-awaited upgrade to a dream property. Whether you are purchasing your first flat or planning your forever home, the journey starts long before you receive the keys.

While saving is essential, relying on cash alone may not be enough in today’s rising property market. A thoughtful investment strategy can help bridge the gap between where you are now and the home you want in the future.

Why Property Ownership Matters So Much in Singapore

Singapore has long been known for its strong property market and high homeownership rate. With over 90% of residents owning a home, property remains one of the most trusted ways to build and preserve wealth locally.

Several factors support this mindset:

Stable economic growth and strong governance

Limited land supply, which supports long-term property values

Property viewed as a tangible and relatively stable asset

That said, affordability has become a growing challenge. Since 2021, both private and public housing prices have risen sharply due to strong demand and supply constraints following the pandemic.

As prices increase faster than wages, planning ahead has never been more important.

Understanding the True Cost of Buying a Home

When buying property in Singapore, the purchase price is only part of the equation. Buyers must also prepare for upfront costs such as:

Minimum 25% down payment for private property

Buyer’s Stamp Duty (BSD)

Legal and administrative fees

Additional Buyer’s Stamp Duty (ABSD), where applicable

For example, a $2 million property can require over $570,000 in upfront cash, even before renovation or furnishing costs. For Singapore Permanent Residents and foreigners, ABSD significantly increases this amount.

This reality highlights why early financial preparation is essential.

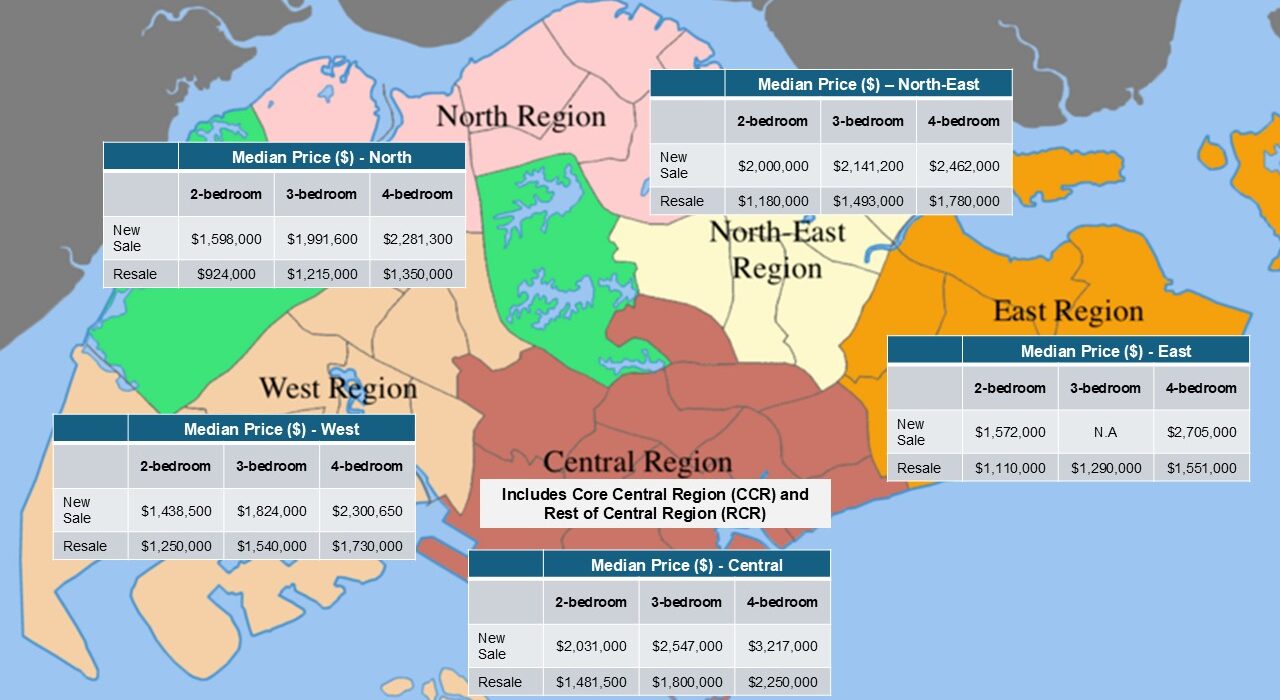

Affordability is often the largest stumbling block when it comes to property. Prices have gained significantly since 2021, driven by the surge in demand and shortage of new homes built as a result of the COVID-19 pandemic. Between 3Q 2021 to 3Q 2025, non-landed private homes and HDB resale prices have risen 30% and 35% respectively.

Table 1: HDB Prices in 4Q 2025

Price Range ($) – BTO (October 2025) | |||

3-room | 4-room | 5-room | |

Standard | $295,000 – $448,000 | $344,000 – $624,000 | $466,000 – $857,000 |

Plus | $340,000 – $434,000 | $514,000 – $650,000 | N.a |

Prime | $408,000 – $552,000 | $541,000 – $778,000 | N.A |

Average Price ($) – Resale | |||

3-room | 4-room | 5-room | |

Mature Estate | $474,000 | $772,000 | $937,000 |

Non-mature Estate | $457,000 | $604,000 | $714,000 |

Source: HDB as of 8 Jan 2026, *Rounded to the nearest ‘000

Why Saving Alone May Not Be Enough

Many aspiring homeowners focus solely on saving for a down payment. While discipline is admirable, cash savings face one major challenge: inflation.

With inflation averaging around 3% annually, money sitting in a low-interest savings account gradually loses purchasing power. Over time, the same amount of cash buys less property, not more.

This creates a gap between rising home prices and stagnant savings, even for consistent savers.

Costs of purchasing a home in Singapore

Property Value | Buyer Stamp Duty | 25% Downpayment* | Legal Fees^ | Total Capital Outlay |

$500,000 | $9,600 | $125,000 | $3,000 | $137,600 |

$750,000 | $17,100 | $187,500 | $3,000 | $207,600 |

$1,000,000 | $24,600 | $250,000 | $3,000 | $277,600 |

$1,500,000 | $44,600 | $375,000 | $3,000 | $422,600 |

$2,000,000 | $69,600 | $500,000 | $3,000 | $572,600 |

$2,500,000 | $94,600 | $625,000 | $3,000 | $722,600 |

$3,000,000 | $119,600 | $750,000 | $3,000 | $872,600 |

$3,500,000 | $149,600 | $875,000 | $3,000 | $1,027,600 |

$4,000,000 | $179,600 | $1,000,000 | $3,000 | $1,182,600 |

$4,500,000 | $209,600 | $1,125,000 | $3,000 | $1,337,600 |

$5,000,000 | $239,600 | $1,250,000 | $3,000 | $1,492,600 |

*Based on minimum down payment ^Estimated amount.

How Investing Helps Close the Gap

Investing allows your money to grow at a faster pace than inflation over the long term. By putting your capital to work in the markets, you give yourself a better chance of keeping up with, or even outpacing property price growth.

Key benefits of investing for homeownership include:

Long-term wealth accumulation through compounding

Higher potential returns compared to cash savings

Flexibility to scale investments as income grows

Starting early makes a powerful difference. Even modest monthly investments can grow substantially over time when compounded consistently.

Building an Investment Strategy for Property Goals

A successful investment plan balances growth and risk. Markets naturally fluctuate, so short-term volatility is unavoidable. However, history shows that staying invested over the long term has rewarded disciplined investors.

To manage risk effectively:

Diversify across asset classes such as equities and bonds

Invest globally rather than relying on a single market

Match your portfolio risk level to your time horizon

A structured, long-term portfolio can support your property goals while reducing emotional decision-making during market swings.

The Power of Regular Investing

For beginners, a recurring investment plan can be a practical starting point. By investing a fixed amount monthly, you benefit from dollar-cost averaging, which helps smooth out market ups and downs over time.

Regular investing also:

Encourages discipline

Reduces the stress of timing the market

Fits naturally into monthly budgeting

As your income increases, you can gradually raise your investment contributions to accelerate progress toward your down payment target.

Laying the Financial Foundation for Your Future Home

Buying a home in Singapore is a long-term journey, not a last-minute decision. By combining smart saving habits with consistent investing, you build a stronger financial foundation and improve your ability to afford the home you truly want.

Whether your goal is your first flat, a larger family home, or a long-term upgrade, starting early and staying invested can make the difference between compromise and choice.

Your dream home is not just about location or layout — it is built on years of thoughtful financial planning.