Singapore stands in a league of its own when it comes to luxury living in Asia. From the gleaming towers of Marina Bay to the quiet, tree-lined boulevards of Nassim and Bukit Timah, luxury homes in Singapore represent the perfect convergence of architectural excellence, world-class lifestyle, and long-term investment strength.

At SG Luxury Condo, we have spent years helping discerning buyers navigate Singapore’s most exclusive residential developments. This guide is built on that expertise. We will walk you through what defines a luxury home in Singapore, where these homes are located, what types of luxury properties exist, how much they cost, who can buy them, and why Singapore continues to attract the world’s most sophisticated property buyers in 2026 and beyond.

What Defines a Luxury Home in Singapore?

The concept of luxury in Singapore’s real estate market has evolved far beyond expensive addresses and marble finishes. In 2026, a true luxury home in Singapore is defined by a combination of location prestige, architectural quality, lifestyle integration, technological sophistication, and long-term value preservation.

From a pricing perspective, properties transacting above SGD 5 million, or those priced at SGD 3,000 per square foot and above, are broadly considered to occupy the luxury bracket. Ultra-premium properties — super penthouses, full-floor apartments, Good Class Bungalows along Nassim Road — regularly trade at SGD 20 million, SGD 30 million, and beyond.

But price alone does not define luxury. The finest high-end real estate in Singapore is distinguished by the following characteristics:

Premium Architecture and Interiors: Luxury homes in Singapore are designed by internationally renowned architects and feature bespoke interiors with Italian marble, engineered timber flooring, floor-to-ceiling glazing, and designer kitchen systems from brands such as Miele, Gaggenau, and Sub-Zero. Every finish, every fitting, and every spatial proportion is the result of intentional design thinking rather than cost efficiency.

Smart Home Technology: The Singapore smart homes market is on a steep growth trajectory, projected to reach USD 7.90 billion by 2025, with smart home adoption having already surged to over 712,200 homes in 2024. In luxury developments, this translates to fully integrated living environments — automated climate control, biometric security systems, AI-powered energy management, and app-controlled home ecosystems that give residents seamless command over every aspect of their home.

Sustainability and Green Credentials: The conversation around luxury has evolved from a focus on opulence alone to a seamless integration of intuitive technology, personal well-being, verifiable sustainability, and impeccable service. Top luxury launches such as River Green — the first private residential development in Singapore to achieve BCA Green Mark Platinum Super Low Energy certification — demonstrate how sustainability has become a core marker of luxury status rather than merely a bonus feature.

Resort-Style Facilities and Services: Infinity pools, private wellness spas, sky terraces, concierge desks, private dining rooms, wine cellars, dedicated car parks, and 24-hour security are standard expectations at the luxury tier. The finest developments go further, offering hotel-style services including housekeeping arrangements, valet parking, and curated resident events.

Exclusivity and Privacy: Many of Singapore’s most coveted luxury developments are deliberately low-density — boutique projects of 30 to 100 units that prioritise privacy, personalised service, and a strong sense of community among like-minded residents.

Location in Prime Districts: Luxury homes in Singapore are almost always found within the Core Central Region, in postal districts that carry enduring prestige, strong connectivity, and proven capital appreciation track records.

Where Are Luxury Homes Located in Singapore?

Singapore’s luxury residential market is anchored within the Core Central Region (CCR) — the collection of prime postal districts that form the island’s most prestigious address zones. Understanding these districts is essential for any buyer seeking the finest high-end real estate Singapore has to offer.

District 9 — Orchard Road and River Valley

District 9 is Singapore’s most iconic luxury address. Orchard Road — the city’s world-famous shopping and lifestyle belt — runs through its centre, while River Valley offers a more intimate, village-like ambience lined with boutique restaurants, wellness studios, and the scenic Singapore River waterfront.

High-end condominiums in District 9 consistently command prices in the range of SGD 2,500 to SGD 3,500 per square foot, with notable luxury launches such as Klimt Cairnhill achieving an average of SGD 3,402 per square foot, and high-value resale transactions such as a unit at Hilltops in District 9 fetching SGD 13 million, demonstrating that buyers are willing to pay a premium for exclusivity and location.

Top luxury condo Singapore developments in District 9 include The Avenir, River Green, Cuscaden Reserve, Klimt Cairnhill, UpperHouse at Orchard Boulevard, and The Robertson Opus. The CCR recorded the strongest performance among all regions in 2026, with prices increasing 1.68% quarter-on-quarter and 8.28% year-on-year, driven in part by notable new launches such as The Robertson Opus, UpperHouse at Orchard Boulevard, and River Green.

District 10 — Bukit Timah, Nassim, Holland Village, and Tanglin

District 10 is the spiritual home of Singapore’s wealthiest families and most senior diplomats. This district carries a quieter, more private character than District 9, with lush greenery, generous land plots, and the highest concentration of Good Class Bungalows on the island.

Nassim Road and Cluny Road are among Singapore’s most coveted addresses, home to embassies, ultra-private residences, and some of the city’s largest remaining freehold land parcels. Luxury condos in District 10 — including The Nassim, Les Maisons Nassim, and Leedon Residence — regularly transact between SGD 2,800 and SGD 4,000 per square foot.

District 11 — Newton, Novena, and Bukit Timah

District 11 is a well-connected prime district that balances residential tranquility with easy access to Singapore’s medical hub, top international schools, and established lifestyle amenities. A notable recent GLS tender for a site near Newton MRT Interchange in prime District 10 attracted eight bids, with the top offer of SGD 566.29 million from HH Investment, reflecting the enduring competition for well-located land in Singapore’s prime residential corridor. Watten House by UOL Group is among the most discussed luxury launches here, offering a refined residential experience on Shelford Road. Prices in District 11 typically range from SGD 2,200 to SGD 3,200 per square foot.

District 1 — Marina Bay and Downtown Core

Marina Bay offers one of the most dramatic luxury living experiences in Asia. Positioned at the heart of Singapore’s financial district and overlooking the iconic Marina Bay Sands, Gardens by the Bay, and the open straits, condominiums here serve a globally mobile professional class who value CBD proximity and an unmistakable address. District 1 homes are ultra-scarce and ultra-expensive, with condo prices averaging over SGD 3,000 per square foot, reflecting the limited availability of skyline homes in developments such as Marina Bay Residences and The Sail.

District 4 — Sentosa Cove and Harbourfront

Sentosa Cove holds a unique and irreplaceable position in Singapore’s luxury property landscape. It is the only location in Singapore where foreign nationals may purchase landed residential property — subject to approval from the Singapore Land Authority. Sentosa Cove is unique as the only place where foreigners can own landed homes with approval, offering resort-style living with properties ranging from SGD 2,500 to SGD 3,500 per square foot. Large waterfront bungalows in Sentosa Cove regularly trade at SGD 10 million to SGD 20 million and above.

Types of Luxury Homes in Singapore

Luxury Condos Singapore

Luxury condominiums are the most accessible and widely available form of high-end real estate in Singapore. These full-facility private developments combine architectural prestige with comprehensive lifestyle amenities and a level of service that rivals the world’s finest hotels.

Singapore’s luxury condo market spans boutique developments of fewer than 50 units — where exclusivity and personalised service are paramount — to larger, full-scale developments offering every conceivable lifestyle facility. Units range from spacious one-bedroom apartments for the globally mobile professional to palatial four- and five-bedroom sky homes designed for multi-generational family living.

The defining characteristics of luxury condos Singapore are resort-quality facilities — infinity pools, sky gyms, spa suites, concierge desks, and private dining rooms — combined with premium branded interiors, smart home systems, and addresses in Singapore’s most prestigious districts. Top luxury condo developments include Klimt Cairnhill, The Robertson Opus, River Green, UpperHouse at Orchard Boulevard, The Avenir, and 21 Anderson in District 10. 21 Anderson, a freehold luxury condo of only 18 units in prime District 10, had four-bedroom units transacting at prices from SGD 20.97 million at SGD 4,672 per square foot to SGD 24 million at SGD 5,347 per square foot.

Landed Property Singapore

Landed homes represent the rarest and most coveted category of residential real estate in Singapore. The term covers a spectrum of property types: terrace houses, semi-detached houses, detached bungalows, and at the very apex, Good Class Bungalows. What unites them is that the owner possesses both the structure and the land it stands on — an extraordinarily scarce privilege in a city-state where land is one of the most tightly controlled resources in Asia.

Landed property Singapore is predominantly restricted to Singapore citizens. Singapore Permanent Residents and foreign nationals require approval from the Singapore Land Authority to purchase mainland landed property, which is rarely granted except in cases of exceptional economic contribution.

For those who desire a landed lifestyle with more shared maintenance responsibilities, strata landed options — cluster houses and townhouses within approved condominium developments — provide an intermediate solution accessible to a wider buyer profile.

Penthouses Singapore

Penthouses are the crown jewel of Singapore’s luxury condominium market. Occupying the highest floors of prime developments, these sky-high residences combine breathtaking panoramic views with expansive floor plans, double-volume ceilings, private rooftop terraces, and dedicated plunge pools.

In Singapore, penthouses are priced at a significant premium above standard units within the same development. A super penthouse in a prime District 9 or District 10 development may span 5,000 to 12,000 square feet, with asking prices ranging from SGD 10 million to SGD 30 million or more, depending on the development, floor level, and view orientation.

Notable penthouses in Singapore include sky suites at Skyline at Orchard Boulevard, duplex apartments at Marina Bay developments, and bespoke full-floor residences at The Nassim. For buyers seeking the ultimate expression of vertical luxury living, penthouses Singapore represent an irreplaceable asset class.

Good Class Bungalows (GCBs)

Good Class Bungalows sit at the absolute pinnacle of Singapore’s residential property hierarchy. There are approximately 2,800 GCBs across 39 gazetted GCB areas in Singapore, with each required to occupy a minimum land area of 1,400 square metres. This extreme scarcity — combined with the fact that GCBs are reserved exclusively for Singapore citizens — ensures they retain an enduring mystique and value that no other property class can match.

The most prestigious GCB areas include Nassim Road, Cluny Park, Dalvey Estate, Chatsworth Park, White House Park, and Victoria Park. These homes are typically owner-occupied by Singapore’s most prominent families and are infrequently traded, making each transaction a significant market event. GCBs regularly transact at SGD 20 million to SGD 80 million and beyond, depending on land size, location, and the quality of the existing or proposed structure.

What Is the Price Range for Luxury Condos in Singapore?

Price transparency is one of Singapore’s greatest strengths as a real estate market. The Urban Redevelopment Authority publishes comprehensive transaction data, allowing buyers to benchmark their purchase decisions with confidence. Here is a clear breakdown of what luxury property costs across Singapore’s prime residential landscape in 2026.

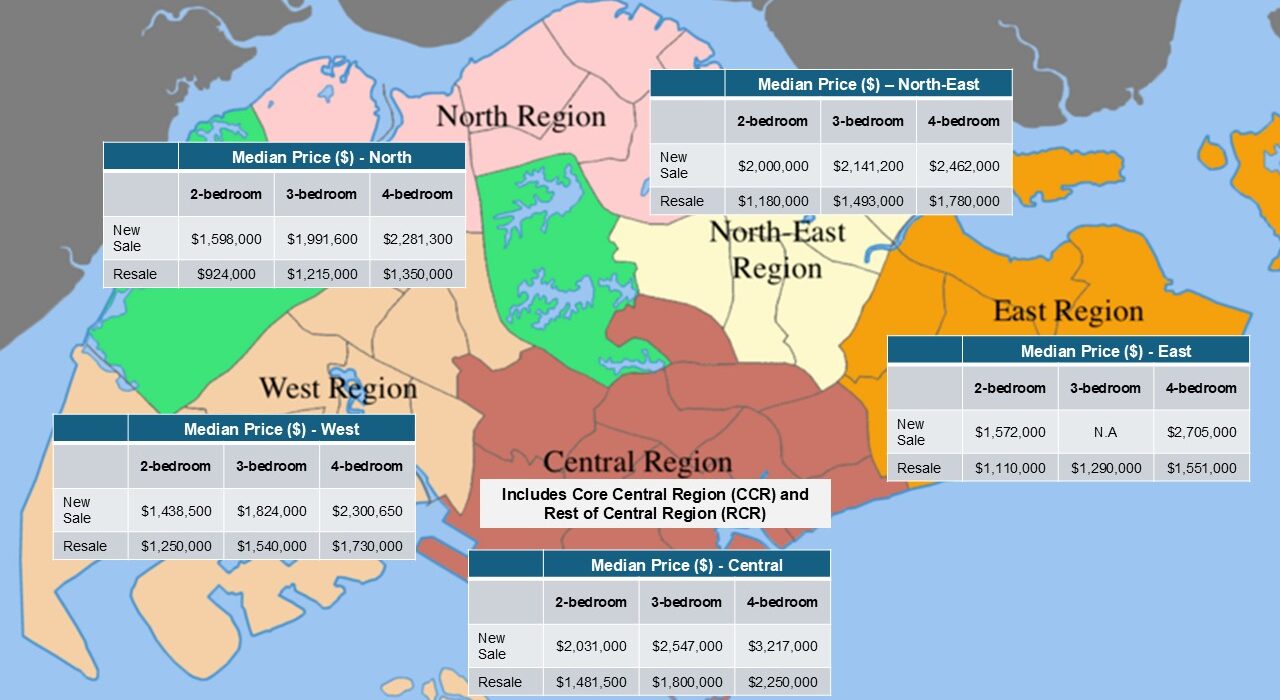

Luxury Condominiums — Core Central Region

For luxury condos in Districts 9, 10, 11, and the Marina Bay area, entry-level pricing begins at approximately SGD 2,000 to SGD 2,500 per square foot. CCR resale prices reached approximately SGD 2,228 per square foot in Q1 2025, while new launches in the region commanded significantly higher premiums.

A two-bedroom luxury condo unit in Districts 9 or 10 typically costs between SGD 3 million and SGD 5 million. Three-bedroom units in prime developments range from SGD 5 million to SGD 8 million. Four-bedroom sky homes, duplex apartments, and larger configurations routinely exceed SGD 10 million.

New Launch vs Resale Pricing

New sales in the CCR averaged SGD 3,208 per square foot in 2026 — the highest among all regions — followed by the Rest of Central Region at SGD 2,695 per square foot and the Outside Central Region at SGD 2,154 per square foot. Buyers willing to purchase resale units in established prime developments can often access properties at a modest discount to new launch pricing, while benefiting from immediate occupancy and proven building quality.

Landed Property Singapore — Price Overview

For landed property Singapore, the price spectrum is wide. A freehold terrace house in a prime district can begin at SGD 5 million to SGD 8 million. Semi-detached houses in Districts 10 and 11 typically range from SGD 8 million to SGD 15 million. Good Class Bungalow average prices moderated to SGD 2,122 per square foot in H1 2025, with 14 GCBs worth SGD 459.63 million transacted in that period. The most prestigious GCBs along Nassim Road and Dalvey Estate can command SGD 30 million to SGD 80 million or more.

Sentosa Cove Landed Homes

Landed properties in Sentosa Cove command premium prices starting from SGD 3 million for basic terrace houses, with luxury detached homes reaching SGD 10 million to SGD 50 million or more.

Stamp Duty Costs — What You Must Budget Beyond the Purchase Price

Every buyer must budget for Buyer’s Stamp Duty (BSD) in addition to the purchase price. BSD follows a tiered structure: 1% on the first SGD 180,000, 2% on the next SGD 180,000, 3% on the next SGD 640,000, and 4% on the next SGD 500,000, stepping up to higher rates for properties above SGD 1.5 million. For a SGD 5 million luxury condo purchase, BSD alone adds approximately SGD 189,600 before any ABSD applies.

Can Foreigners Buy Luxury Property in Singapore?

This is one of the most frequently asked questions from international buyers considering Singapore’s high-end real estate market, and the answer requires careful nuance.

Private Condominiums — Open to All Foreign Buyers

Foreigners can purchase private condominiums and apartments freely in Singapore, but cannot purchase landed property without special approval from the Singapore Land Authority. This makes luxury condos Singapore the primary and most practical entry point for international buyers.

However, foreign buyers must account for the Additional Buyer’s Stamp Duty (ABSD). Any residential property purchased by a foreigner is subject to a flat 60% ABSD, regardless of whether it is the first property, meaning a foreign buyer purchasing a SGD 1 million condominium will pay SGD 600,000 in ABSD alone.

In practical terms, a SGD 2 million condo purchase by a foreign buyer incurs SGD 64,600 in BSD and SGD 1.2 million in ABSD, bringing total tax obligations to over SGD 1.26 million on top of the purchase price.

ABSD Exemptions — FTA Countries

Citizens of countries that have signed Free Trade Agreements with Singapore may qualify for ABSD remission, allowing them to be treated equivalently to Singapore citizens for stamp duty purposes. These countries include the United States of America, Iceland, Liechtenstein, Norway, and Switzerland. Buyers from these countries should confirm their eligibility with a qualified conveyancing lawyer before proceeding.

Landed Property — Mainland Singapore

Foreign nationals generally cannot buy landed property in Singapore unless they have special approval from the Singapore Land Authority, and this approval is rarely granted except in cases of exceptional economic contribution to Singapore. For most foreign buyers, mainland landed property in Singapore remains out of reach regardless of financial capacity.

Sentosa Cove — The Exception for Foreigner Landed Purchases

Sentosa Cove is a gazetted exception to Singapore’s Residential Property Act rules on foreign ownership of landed property. It was specifically designed to attract high-net-worth foreign individuals, and the approval process for Sentosa Cove properties is significantly more streamlined than for mainland properties.

Foreigners buying landed properties at Sentosa Cove must still seek approval from the Land Dealings Approval Unit, and the property must be used solely for the owner’s own occupation and that of their family as a dwelling house, not for rental or any other purpose. Additionally, the land area of the property must not exceed 1,800 square metres, and foreigners can only own one restricted property at a time.

Permanent Residents

Singapore Permanent Residents occupy a middle ground. They may purchase private condominiums freely, and may apply to purchase mainland landed property — though approval is similarly rare and subject to evaluation of their economic contribution and long-term commitment to Singapore. PRs pay a 5% ABSD on their first residential property purchase and higher rates on subsequent purchases.

Singapore Luxury Property Market Trends 2026

Singapore’s luxury property market in 2026 is not merely resilient — it is performing with genuine momentum across multiple segments. Understanding the data behind this performance is essential for any buyer or investor making decisions in this space.

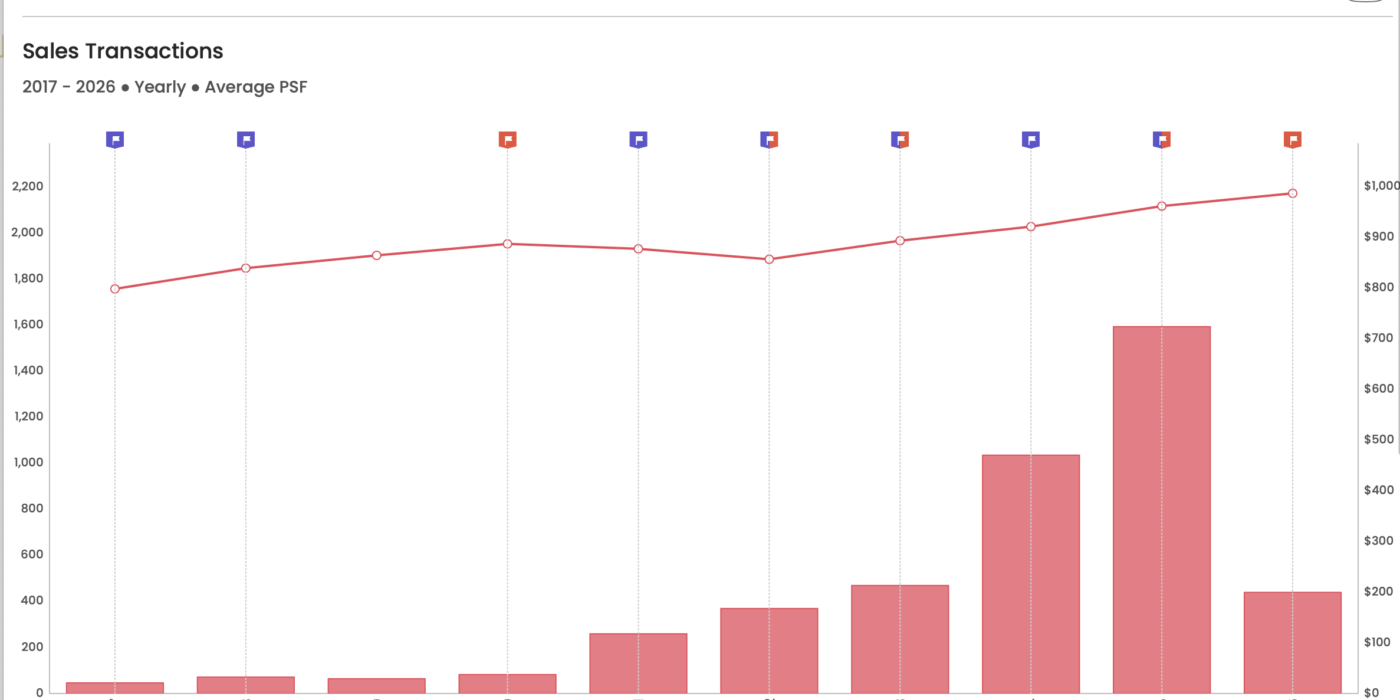

Private residential sales activity in Singapore strengthened considerably, with 7,404 residential units transacted in Q3 206, marking a robust 37.83% increase year-on-year. Total sales for the first three quarters of the year reached 19,793 units, up 36.34% from the same period in 2024.

At the luxury tier specifically, luxury apartment sales surged in H1 2025, with 45 units transacted for SGD 584.26 million — up 155.8% half-on-half and 53.9% year-on-year, with the average price rising 6.2% to SGD 3,736 per square foot.

The CCR Resurgence

2026 was a defining year for Singapore’s Core Central Region. Almost a quarter of all new launches were located in this prime residential zone, which comprises several prime residential districts catering to affluent locals and well-heeled foreign investors. Developers found renewed confidence from strong sales despite a relatively higher price per square foot.

The CCR recorded the strongest performance among all regions, with prices increasing 1.68% quarter-on-quarter and 8.28% year-on-year, driven by notable new launches such as The Robertson Opus, UpperHouse at Orchard Boulevard, and River Green.

Wealthy Singaporeans and PRs Lead Demand

In lieu of foreign buyers who have stayed away from the private home market due to the 60% ABSD rate, wealthy Singaporeans and Permanent Residents have been actively seeking investment opportunities in Singapore’s prime residential areas. This domestic demand from affluent local buyers has provided a stable and deep demand base for the CCR market, replacing some of the foreign buyer activity lost since the April 2023 ABSD revision.

Price Growth Outlook

Forecasts by CBRE, Knight Frank, OrangeTee, and PropNex place 2026 price growth in the range of 3% to 5%. Looking beyond 2026, OrangeTee has stated that as interest rates continue to moderate, high-net-worth individuals seeking capital preservation may continue to invest in luxury landed properties, and buying appetite for luxury apartments is expected to continue into 2026.

Mixed-Use Luxury Developments

Mixed-use developments are gaining traction by integrating condo units with commercial and retail space, enabling residents to take the lift directly from home to shopping and dining areas. Developments like One Holland Village and The Reserve Residences in Bukit Timah provide integrated residential, retail, and office spaces to meet the needs of contemporary buyers who are looking for holistic lifestyle choices.

Step-by-Step Guide to Buying a Luxury Home in Singapore

Step 1 — Establish Your Eligibility and Total Budget

Before beginning your property search, confirm what you are eligible to purchase based on your citizenship or residency status. Singapore citizens have the widest access, Permanent Residents have slightly more restricted access, and foreign nationals are limited to private condominiums and Sentosa Cove landed homes.

Step 2 — Engage a Specialist Property Consultant and Conveyancing Lawyer

In Singapore’s luxury market, working with an experienced specialist who knows the prime districts deeply is essential. The right consultant will give you access to listings before they reach the open market, provide accurate comparable data, and advise you on which developments offer the best long-term value for your specific needs.

Simultaneously, appoint a conveyancing lawyer early. A critical deadline arises at the stage of exercising the Option to Purchase: you must pay your BSD and any applicable ABSD to the Inland Revenue Authority of Singapore within 14 days of signing the Sale and Purchase Agreement. Failure to pay on time incurs penalties.

Step 3 — Secure the Option to Purchase

Once you identify the right property and agree on a price with the seller, you will be issued an Option to Purchase (OTP) upon payment of an option fee — typically 1% of the purchase price. This gives you the exclusive right to purchase within the option period, during which the seller cannot sell to any other buyer.

Exercise the OTP by paying a further 4% exercise fee within the option period. Your lawyer will simultaneously lodge a caveat with the Singapore Land Authority to protect your interest in the property.

Step 4 — Pay Stamp Duties

BSD and any applicable ABSD must be paid within 14 days of exercising the Option to Purchase. The final stage of the transaction is Completion Day, which is typically scheduled 8 to 12 weeks after the exercising of the OTP, when the bank disburses the loan, all funds are transferred, and legal ownership of the property is officially transferred to the buyer’s name and registered with the Singapore Land Authority.

Step 5 — Secure Financing

Singapore’s banks offer mortgage facilities of up to 75% of the property’s valuation for a first residential purchase, subject to the Monetary Authority of Singapore’s Loan-to-Value framework. Foreign buyers may face stricter LTV ratios and should obtain an In-Principle Approval from a bank before committing to a purchase. Rental yields for luxury condos in central locations such as Orchard, Marina Bay, and Sentosa average 3% to 4% gross, which many buyers factor into their financing calculations.

Step 6 — Final Inspection and Key Collection

Before completion, conduct a thorough inspection of the property. For resale luxury homes, verify all fixtures, fittings, and systems. For new launch developments, your developer will provide a Defects Liability Period during which they are obligated to rectify any defects identified at handover.

Why Singapore Is Asia’s Most Coveted Address for Luxury Living

Beyond the transaction mechanics and price data, there is a deeper story that explains why Singapore consistently attracts the world’s most discerning property buyers. This is ultimately the foundation on which the value of luxury homes in Singapore rests.

Political Stability and Property Rights

- A True Global Hub

- World-Class Education, Healthcare, and Lifestyle

- Structural Land Scarcity

- A Track Record of Resilience

Conclusion: Your Gateway to Luxury Homes Singapore

Singapore’s luxury property market in 2026 offers a rare combination: genuine lifestyle excellence, ironclad legal protections, structural supply scarcity, and a long-term track record of value creation that few property markets anywhere in the world can match.

Whether you are searching for a prestigious luxury condo Singapore in the heart of Orchard Road, a tranquil landed property Singapore on the leafy streets of Bukit Timah, a jaw-dropping penthouse Singapore overlooking Marina Bay, or an exclusive waterfront bungalow at Sentosa Cove — SG Luxury Condo is your trusted guide to Singapore’s finest residential real estate.

Contact SG Luxury Condo today for a private, no-obligation consultation. Your ideal luxury home in Singapore is closer than you think.

![Tanjong Rhu Close 505 Units (RCR, City Fringe) [Must-Watch]](https://sgluxurycondo.com/wp-content/uploads/2026/06/Tanjong-Rhu-Close-505-Units-RCR-City-Fringe-Must-Watch.png)